Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeConformal k-NN Anomaly Detector for Univariate Data Streams

Paper and Code

Jun 11, 2017

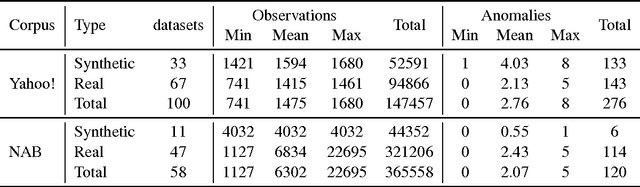

Anomalies in time-series data give essential and often actionable information in many applications. In this paper we consider a model-free anomaly detection method for univariate time-series which adapts to non-stationarity in the data stream and provides probabilistic abnormality scores based on the conformal prediction paradigm. Despite its simplicity the method performs on par with complex prediction-based models on the Numenta Anomaly Detection benchmark and the Yahoo! S5 dataset.

* 15 pages, 2 figures, 7 tables

View paper on