Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeConformal Inference for Online Prediction with Arbitrary Distribution Shifts

Paper and Code

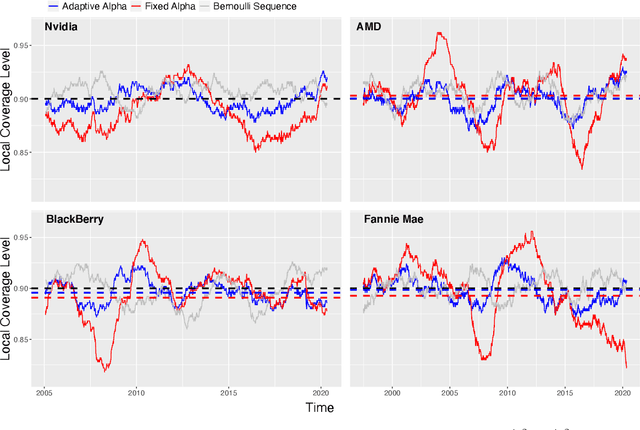

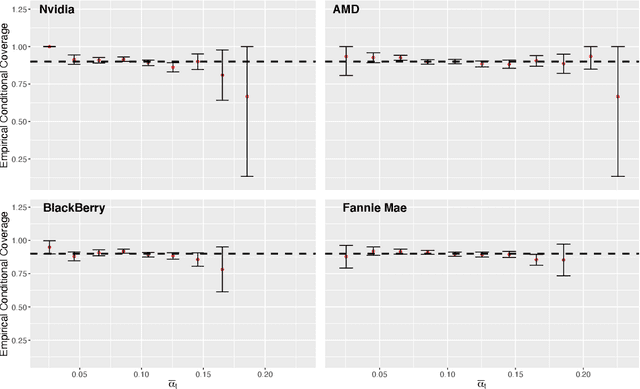

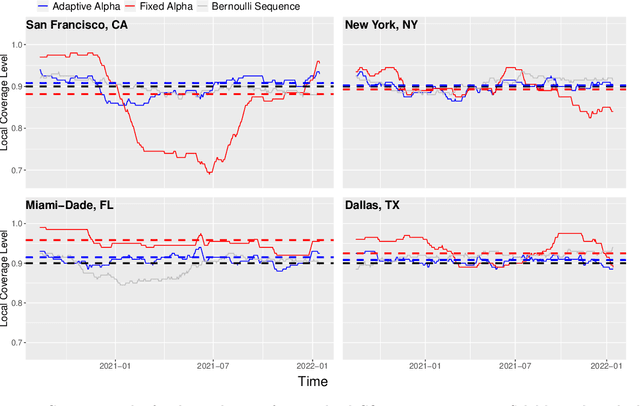

Conformal inference is a flexible methodology for transforming the predictions made by any black-box model (e.g. neural nets, random forests) into valid prediction sets. The only necessary assumption is that the training and test data be exchangeable (e.g. i.i.d.). Unfortunately, this assumption is usually unrealistic in online environments in which the processing generating the data may vary in time and consecutive data-points are often temporally correlated. In this article, we develop an online algorithm for producing prediction intervals that are robust to these deviations. Our methods build upon conformal inference and thus can be combined with any black-box predictor. We show that the coverage error of our algorithm is controlled by the size of the underlying change in the environment and thus directly connect the size of the distribution shift with the difficulty of the prediction problem. Finally, we apply our procedure in two real-world settings and find that our method produces robust prediction intervals under real-world dynamics.