Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeConditional Mutual information-based Contrastive Loss for Financial Time Series Forecasting

Paper and Code

Feb 18, 2020

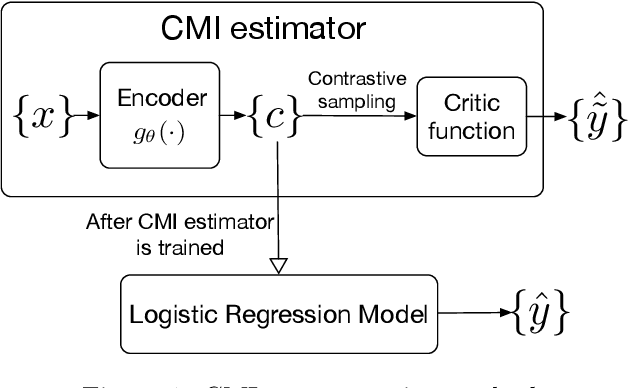

We present a method for financial time series forecasting using representation learning techniques. Recent progress on deep autoregressive models has shown their ability to capture long-term dependencies of the sequence data. However, the shortage of available financial data for training will make the deep models susceptible to the overfitting problem. In this paper, we propose a neural-network-powered conditional mutual information (CMI) estimator for learning representations for the forecasting task. Specifically, we first train an encoder to maximize the mutual information between the latent variables and the label information conditioned on the encoded observed variables. Then the features extracted from the trained encoder are used to learn a subsequent logistic regression model for predicting time series movements. Our proposed estimator transforms the CMI maximization problem to a classification problem whether two encoded representations are sampled from the same class or not. This is equivalent to perform pairwise comparisons of the training datapoints, and thus, improves the generalization ability of the deep autoregressive model. Empirical experiments indicate that our proposed method has the potential to advance the state-of-the-art performance.