Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeCNNPred: CNN-based stock market prediction using several data sources

Paper and Code

Oct 21, 2018

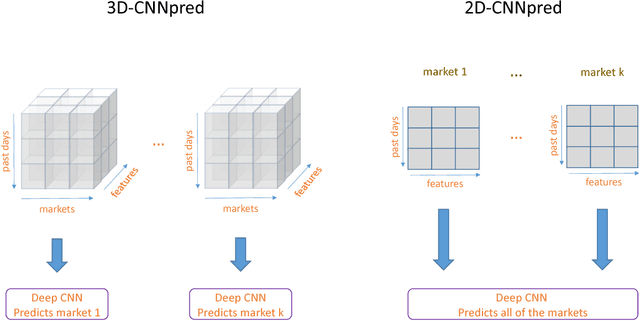

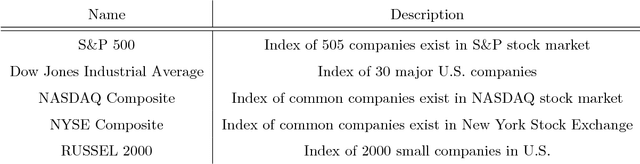

Feature extraction from financial data is one of the most important problems in market prediction domain for which many approaches have been suggested. Among other modern tools, convolutional neural networks (CNN) have recently been applied for automatic feature selection and market prediction. However, in experiments reported so far, less attention has been paid to the correlation among different markets as a possible source of information for extracting features. In this paper, we suggest a CNN-based framework with specially designed CNNs, that can be applied on a collection of data from a variety of sources, including different markets, in order to extract features for predicting the future of those markets. The suggested framework has been applied for predicting the next day's direction of movement for the indices of S&P 500, NASDAQ, DJI, NYSE, and RUSSELL markets based on various sets of initial features. The evaluations show a significant improvement in prediction's performance compared to the state of the art baseline algorithms.