Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeCNN-based Realized Covariance Matrix Forecasting

Paper and Code

Jul 22, 2021

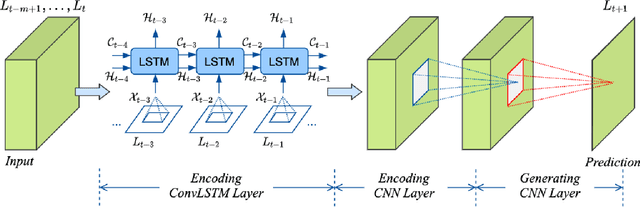

It is well known that modeling and forecasting realized covariance matrices of asset returns play a crucial role in the field of finance. The availability of high frequency intraday data enables the modeling of the realized covariance matrices directly. However, most of the models available in the literature depend on strong structural assumptions and they often suffer from the curse of dimensionality. We propose an end-to-end trainable model built on the CNN and Convolutional LSTM (ConvLSTM) which does not require to make any distributional or structural assumption but could handle high-dimensional realized covariance matrices consistently. The proposed model focuses on local structures and spatiotemporal correlations. It learns a nonlinear mapping that connect the historical realized covariance matrices to the future one. Our empirical studies on synthetic and real-world datasets demonstrate its excellent forecasting ability compared with several advanced volatility models.