Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeClustering Time Series Data with Gaussian Mixture Embeddings in a Graph Autoencoder Framework

Paper and Code

Nov 25, 2024

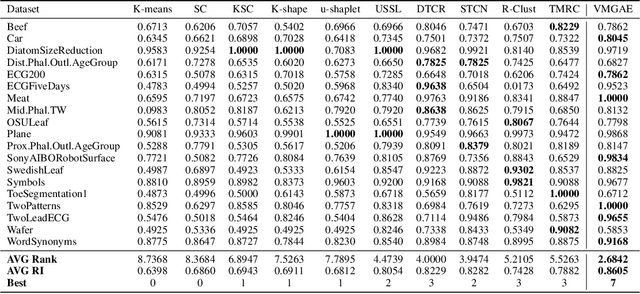

Time series data analysis is prevalent across various domains, including finance, healthcare, and environmental monitoring. Traditional time series clustering methods often struggle to capture the complex temporal dependencies inherent in such data. In this paper, we propose the Variational Mixture Graph Autoencoder (VMGAE), a graph-based approach for time series clustering that leverages the structural advantages of graphs to capture enriched data relationships and produces Gaussian mixture embeddings for improved separability. Comparisons with baseline methods are included with experimental results, demonstrating that our method significantly outperforms state-of-the-art time-series clustering techniques. We further validate our method on real-world financial data, highlighting its practical applications in finance. By uncovering community structures in stock markets, our method provides deeper insights into stock relationships, benefiting market prediction, portfolio optimization, and risk management.