Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeClustering in Recurrent Neural Networks for Micro-Segmentation using Spending Personality

Paper and Code

Oct 13, 2021

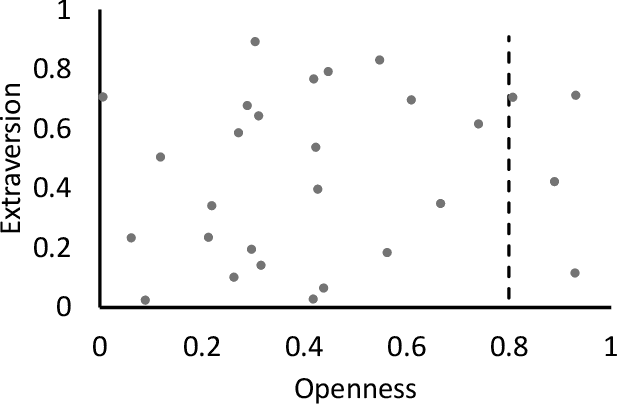

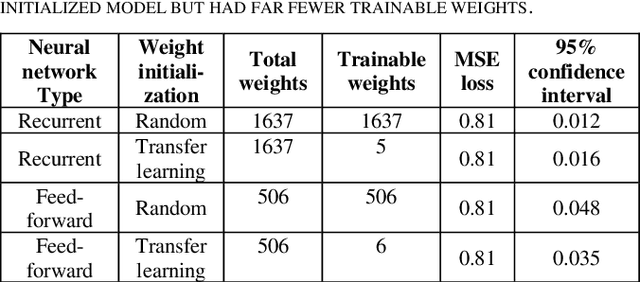

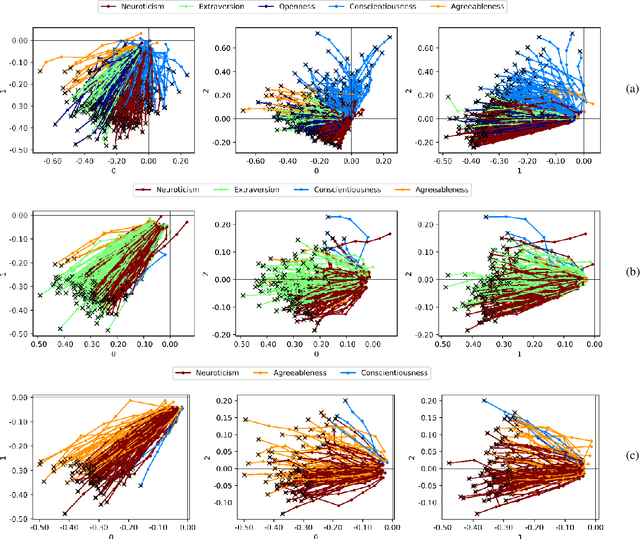

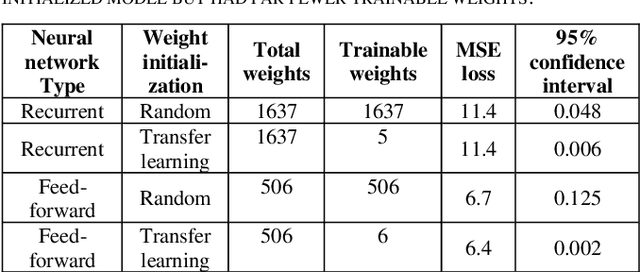

Customer segmentation has long been a productive field in banking. However, with new approaches to traditional problems come new opportunities. Fine-grained customer segments are notoriously elusive and one method of obtaining them is through feature extraction. It is possible to assign coefficients of standard personality traits to financial transaction classes aggregated over time. However, we have found that the clusters formed are not sufficiently discriminatory for micro-segmentation. In a novel approach, we extract temporal features with continuous values from the hidden states of neural networks predicting customers' spending personality from their financial transactions. We consider both temporal and non-sequential models, using long short-term memory (LSTM) and feed-forward neural networks, respectively. We found that recurrent neural networks produce micro-segments where feed-forward networks produce only coarse segments. Finally, we show that classification using these extracted features performs at least as well as bespoke models on two common metrics, namely loan default rate and customer liquidity index.