Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeChaotic Hedging with Iterated Integrals and Neural Networks

Paper and Code

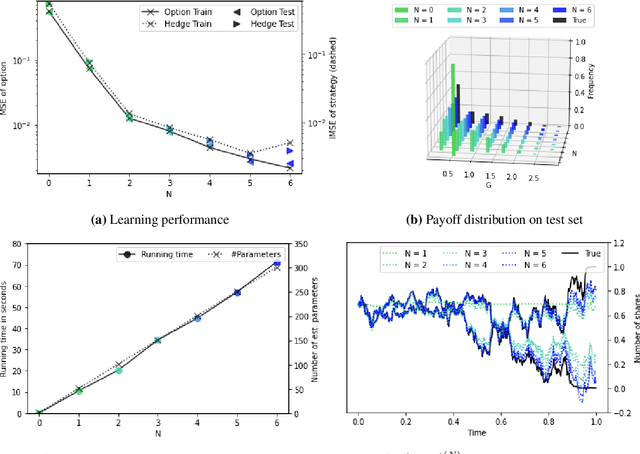

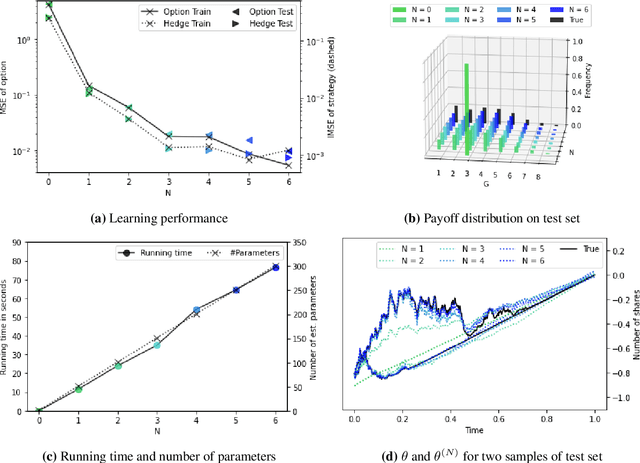

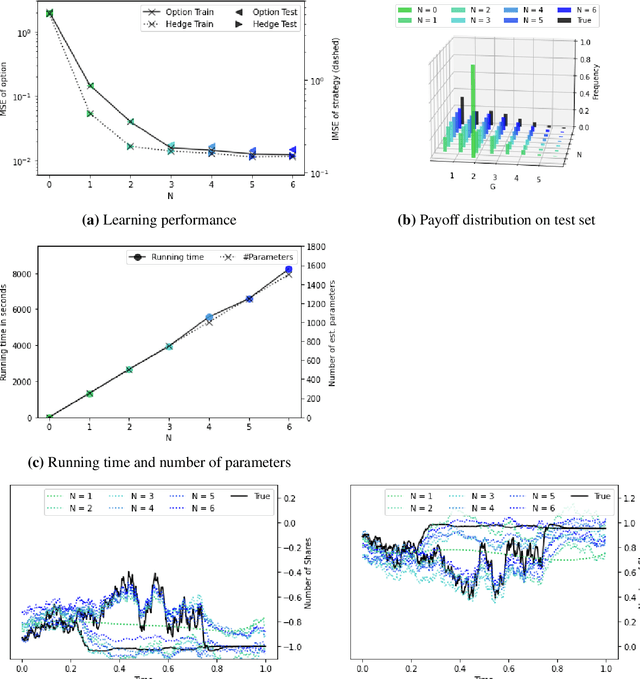

In this paper, we extend the Wiener-Ito chaos decomposition to the class of diffusion processes, whose drift and diffusion coefficient are of linear growth. By omitting the orthogonality in the chaos expansion, we are able to show that every $p$-integrable functional, for $p \in [1,\infty)$, can be represented as sum of iterated integrals of the underlying process. Using a truncated sum of this expansion and (possibly random) neural networks for the integrands, whose parameters are learned in a machine learning setting, we show that every financial derivative can be approximated arbitrarily well in the $L^p$-sense. Moreover, the hedging strategy of the approximating financial derivative can be computed in closed form.

View paper on