Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeBayesian nonparametric multivariate convex regression

Paper and Code

Sep 01, 2011

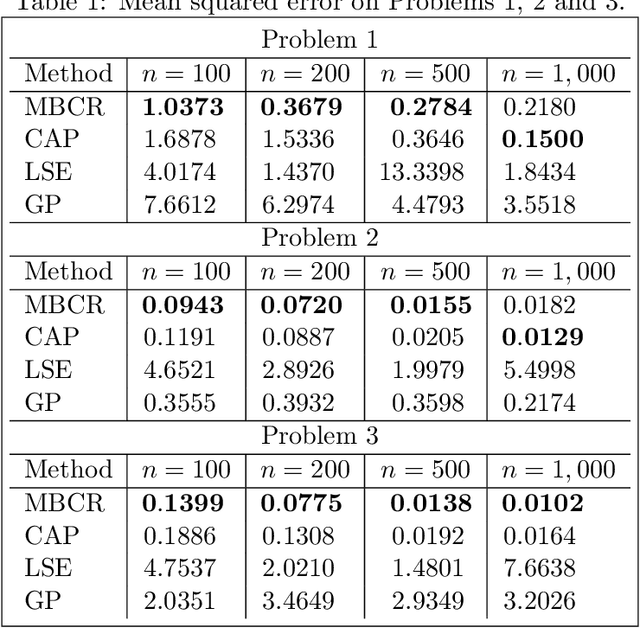

In many applications, such as economics, operations research and reinforcement learning, one often needs to estimate a multivariate regression function f subject to a convexity constraint. For example, in sequential decision processes the value of a state under optimal subsequent decisions may be known to be convex or concave. We propose a new Bayesian nonparametric multivariate approach based on characterizing the unknown regression function as the max of a random collection of unknown hyperplanes. This specification induces a prior with large support in a Kullback-Leibler sense on the space of convex functions, while also leading to strong posterior consistency. Although we assume that f is defined over R^p, we show that this model has a convergence rate of log(n)^{-1} n^{-1/(d+2)} under the empirical L2 norm when f actually maps a d dimensional linear subspace to R. We design an efficient reversible jump MCMC algorithm for posterior computation and demonstrate the methods through application to value function approximation.