Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeAssessing Robustness of Machine Learning Models using Covariate Perturbations

Paper and Code

Aug 02, 2024

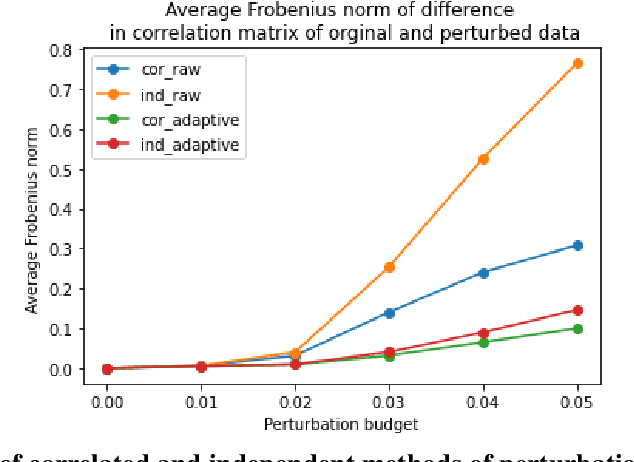

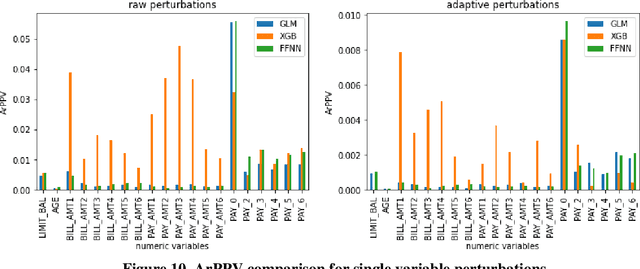

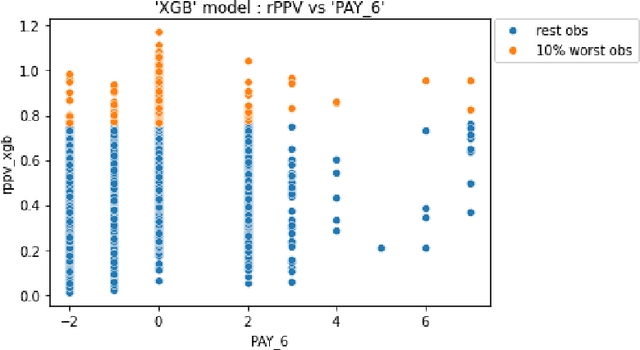

As machine learning models become increasingly prevalent in critical decision-making models and systems in fields like finance, healthcare, etc., ensuring their robustness against adversarial attacks and changes in the input data is paramount, especially in cases where models potentially overfit. This paper proposes a comprehensive framework for assessing the robustness of machine learning models through covariate perturbation techniques. We explore various perturbation strategies to assess robustness and examine their impact on model predictions, including separate strategies for numeric and non-numeric variables, summaries of perturbations to assess and compare model robustness across different scenarios, and local robustness diagnosis to identify any regions in the data where a model is particularly unstable. Through empirical studies on real world dataset, we demonstrate the effectiveness of our approach in comparing robustness across models, identifying the instabilities in the model, and enhancing model robustness.