Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeAn Interpretable and Efficient Infinite-Order Vector Autoregressive Model for High-Dimensional Time Series

Paper and Code

Sep 16, 2022

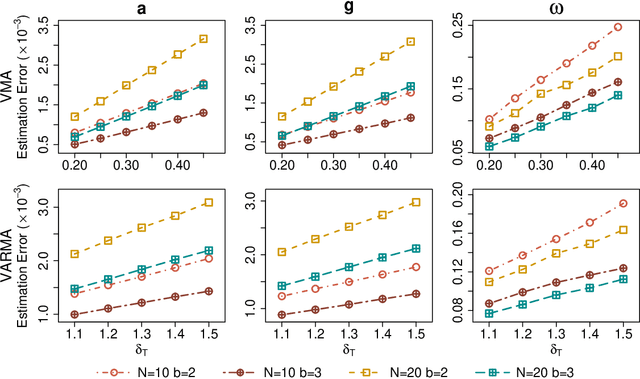

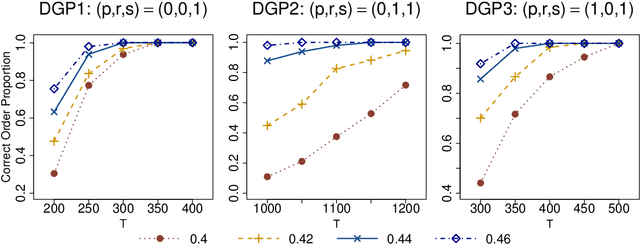

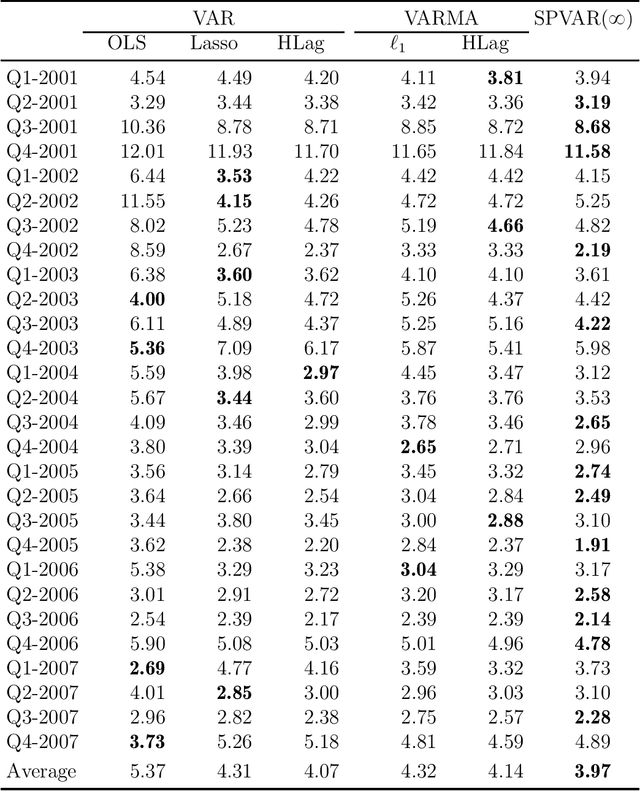

As a special infinite-order vector autoregressive (VAR) model, the vector autoregressive moving average (VARMA) model can capture much richer temporal patterns than the widely used finite-order VAR model. However, its practicality has long been hindered by its non-identifiability, computational intractability, and relative difficulty of interpretation. This paper introduces a novel infinite-order VAR model which, with only a little sacrifice of generality, inherits the essential temporal patterns of the VARMA model but avoids all of the above drawbacks. As another attractive feature, the temporal and cross-sectional dependence structures of this model can be interpreted separately, since they are characterized by different sets of parameters. For high-dimensional time series, this separation motivates us to impose sparsity on the parameters determining the cross-sectional dependence. As a result, greater statistical efficiency and interpretability can be achieved, while no loss of temporal information is incurred by the imposed sparsity. We introduce an $\ell_1$-regularized estimator for the proposed model and derive the corresponding nonasymptotic error bounds. An efficient block coordinate descent algorithm and a consistent model order selection method are developed. The merit of the proposed approach is supported by simulation studies and a real-world macroeconomic data analysis.