Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeA Worrying Analysis of Probabilistic Time-series Models for Sales Forecasting

Paper and Code

Nov 21, 2020

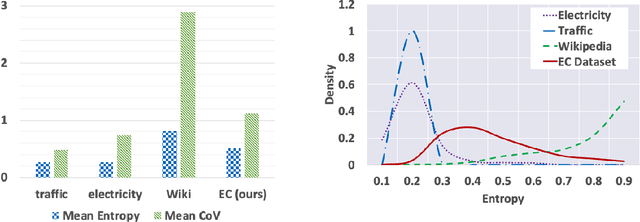

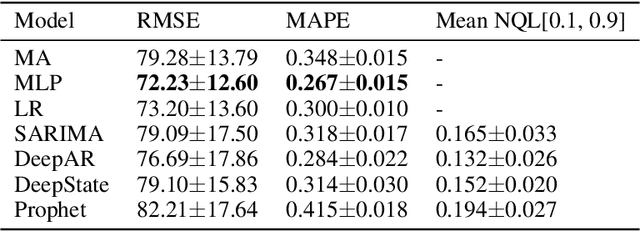

Probabilistic time-series models become popular in the forecasting field as they help to make optimal decisions under uncertainty. Despite the growing interest, a lack of thorough analysis hinders choosing what is worth applying for the desired task. In this paper, we analyze the performance of three prominent probabilistic time-series models for sales forecasting. To remove the role of random chance in architecture's performance, we make two experimental principles; 1) Large-scale dataset with various cross-validation sets. 2) A standardized training and hyperparameter selection. The experimental results show that a simple Multi-layer Perceptron and Linear Regression outperform the probabilistic models on RMSE without any feature engineering. Overall, the probabilistic models fail to achieve better performance on point estimation, such as RMSE and MAPE, than comparably simple baselines. We analyze and discuss the performances of probabilistic time-series models.