Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeA Neural RDE-based model for solving path-dependent PDEs

Paper and Code

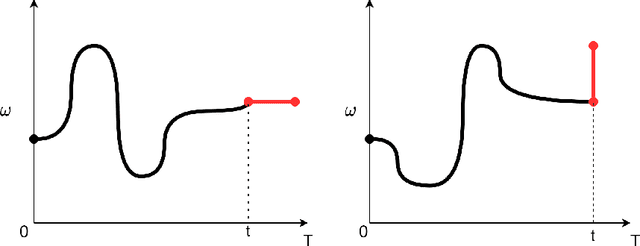

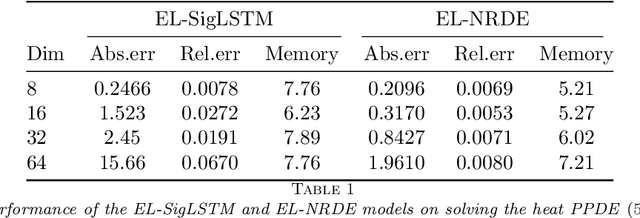

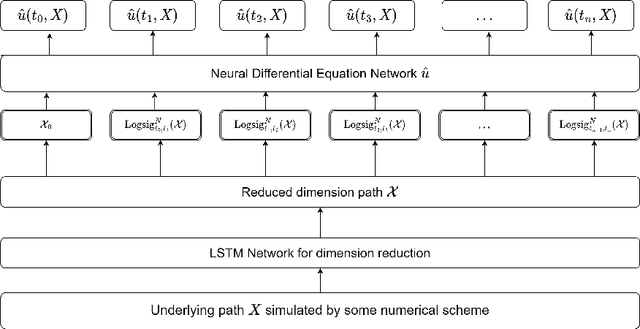

The concept of the path-dependent partial differential equation (PPDE) was first introduced in the context of path-dependent derivatives in financial markets. Its semilinear form was later identified as a non-Markovian backward stochastic differential equation (BSDE). Compared to the classical PDE, the solution of a PPDE involves an infinite-dimensional spatial variable, making it challenging to approximate, if not impossible. In this paper, we propose a neural rough differential equation (NRDE)-based model to learn PPDEs, which effectively encodes the path information through the log-signature feature while capturing the fundamental dynamics. The proposed continuous-time model for the PPDE solution offers the benefits of efficient memory usage and the ability to scale with dimensionality. Several numerical experiments, provided to validate the performance of the proposed model in comparison to the strong baseline in the literature, are used to demonstrate its effectiveness.