Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeA Multi-criteria Approach to Evolve Sparse Neural Architectures for Stock Market Forecasting

Paper and Code

Nov 15, 2021

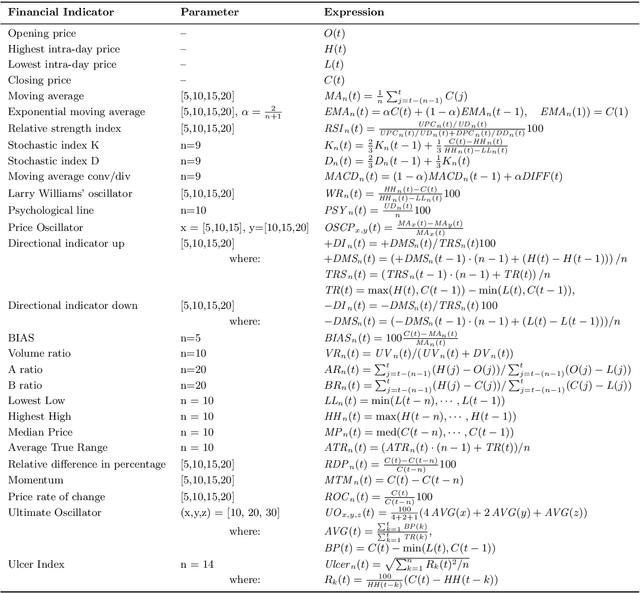

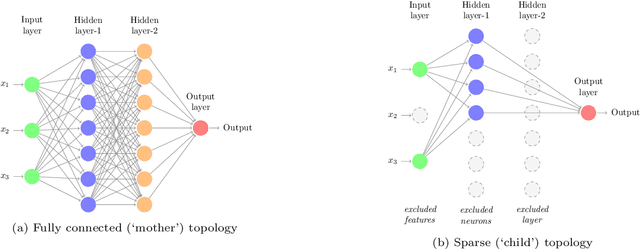

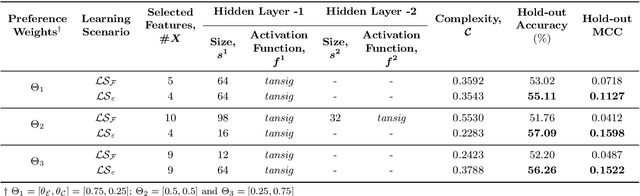

This study proposes a new framework to evolve efficacious yet parsimonious neural architectures for the movement prediction of stock market indices using technical indicators as inputs. In the light of a sparse signal-to-noise ratio under the Efficient Market hypothesis, developing machine learning methods to predict the movement of a financial market using technical indicators has shown to be a challenging problem. To this end, the neural architecture search is posed as a multi-criteria optimization problem to balance the efficacy with the complexity of architectures. In addition, the implications of different dominant trading tendencies which may be present in the pre-COVID and within-COVID time periods are investigated. An $\epsilon-$ constraint framework is proposed as a remedy to extract any concordant information underlying the possibly conflicting pre-COVID data. Further, a new search paradigm, Two-Dimensional Swarms (2DS) is proposed for the multi-criteria neural architecture search, which explicitly integrates sparsity as an additional search dimension in particle swarms. A detailed comparative evaluation of the proposed approach is carried out by considering genetic algorithm and several combinations of empirical neural design rules with a filter-based feature selection method (mRMR) as baseline approaches. The results of this study convincingly demonstrate that the proposed approach can evolve parsimonious networks with better generalization capabilities.