Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeA Modularized and Scalable Multi-Agent Reinforcement Learning-based System for Financial Portfolio Management

Paper and Code

Feb 09, 2021

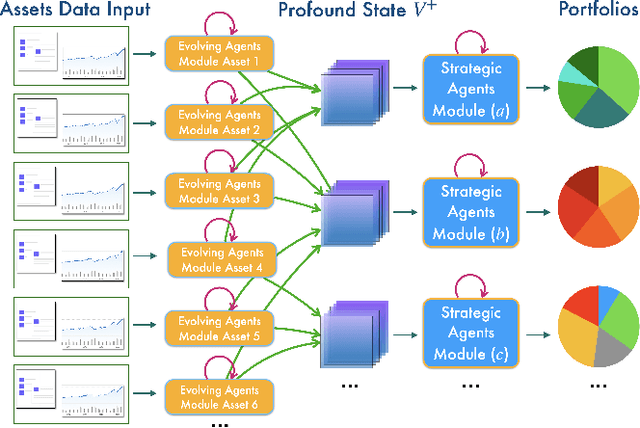

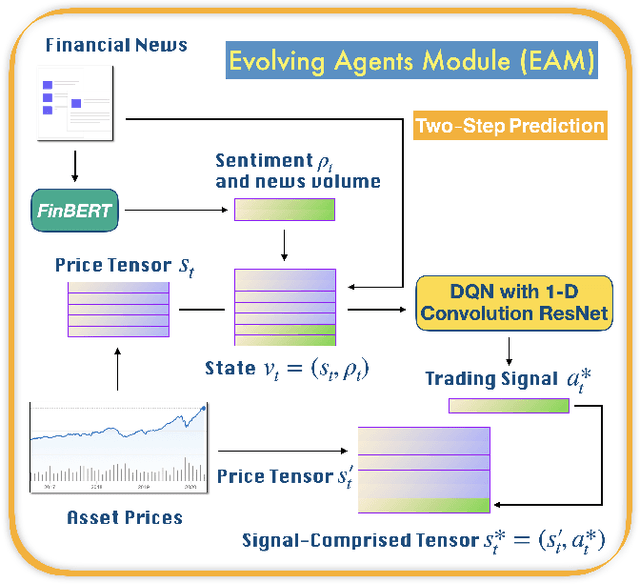

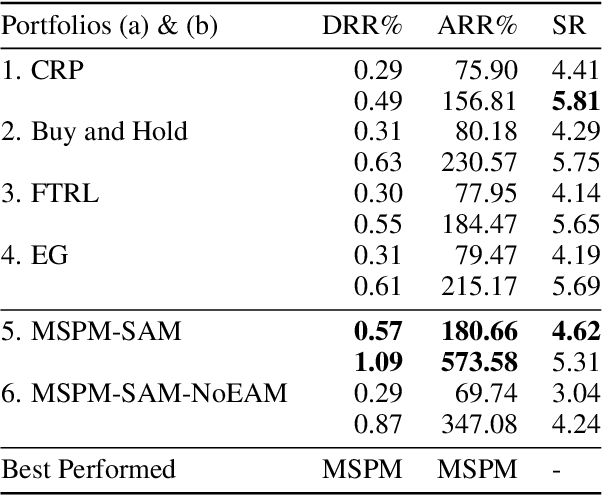

Financial Portfolio Management is one of the most applicable problems in Reinforcement Learning (RL) by its sequential decision-making nature. Existing RL-based approaches, while inspiring, often lack scalability, reusability, or profundity of intake information to accommodate the ever-changing capital markets. In this paper, we design and develop MSPM, a novel Multi-agent Reinforcement learning-based system with a modularized and scalable architecture for portfolio management. MSPM involves two asynchronously updated units: Evolving Agent Module (EAM) and Strategic Agent Module (SAM). A self-sustained EAM produces signal-comprised information for a specific asset using heterogeneous data inputs, and each EAM possesses its reusability to have connections to multiple SAMs. A SAM is responsible for the assets reallocation of a portfolio using profound information from the EAMs connected. With the elaborate architecture and the multi-step condensation of the volatile market information, MSPM aims to provide a customizable, stable, and dedicated solution to portfolio management that existing approaches do not. We also tackle data-shortage issue of newly-listed stocks by transfer learning, and validate the necessity of EAM. Experiments on 8-year U.S. stock markets data prove the effectiveness of MSPM in profits accumulation by its outperformance over existing benchmarks.