Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDominant Shuffle: A Simple Yet Powerful Data Augmentation for Time-series Prediction

May 26, 2024

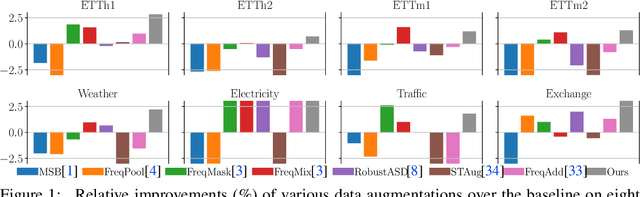

Recent studies have suggested frequency-domain Data augmentation (DA) is effec tive for time series prediction. Existing frequency-domain augmentations disturb the original data with various full-spectrum noises, leading to excess domain gap between augmented and original data. Although impressive performance has been achieved in certain cases, frequency-domain DA has yet to be generalized to time series prediction datasets. In this paper, we found that frequency-domain augmentations can be significantly improved by two modifications that limit the perturbations. First, we found that limiting the perturbation to only dominant frequencies significantly outperforms full-spectrum perturbations. Dominant fre quencies represent the main periodicity and trends of the signal and are more important than other frequencies. Second, we found that simply shuffling the dominant frequency components is superior over sophisticated designed random perturbations. Shuffle rearranges the original components (magnitudes and phases) and limits the external noise. With these two modifications, we proposed dominant shuffle, a simple yet effective data augmentation for time series prediction. Our method is very simple yet powerful and can be implemented with just a few lines of code. Extensive experiments with eight datasets and six popular time series models demonstrate that our method consistently improves the baseline performance under various settings and significantly outperforms other DA methods. Code can be accessed at https://kaizhao.net/time-series.