Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeStatistical Inference for Weighted Sample Average Approximation in Contextual Stochastic Optimization

Mar 17, 2025

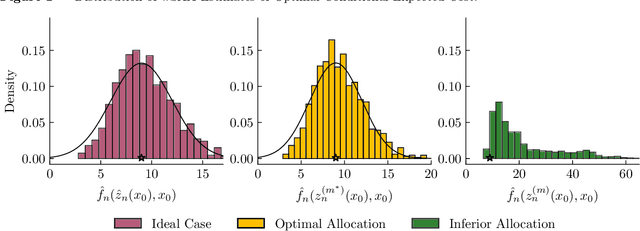

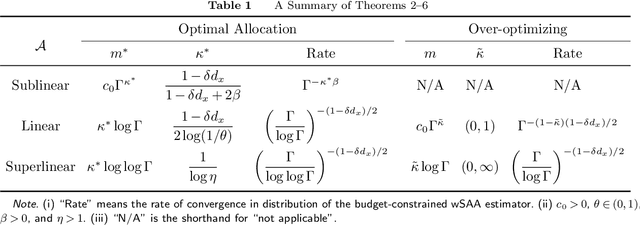

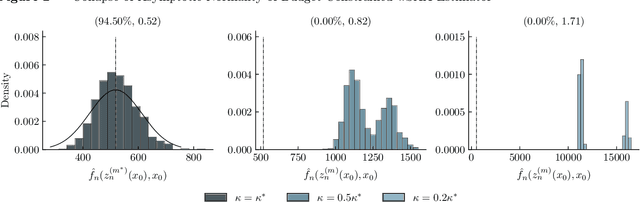

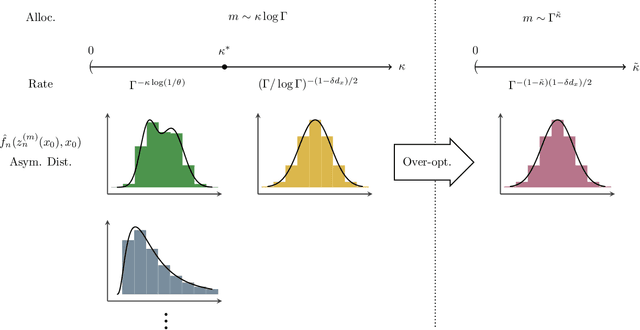

Contextual stochastic optimization provides a framework for decision-making under uncertainty incorporating observable contextual information through covariates. We analyze statistical inference for weighted sample average approximation (wSAA), a widely-used method for solving contextual stochastic optimization problems. We first establish central limit theorems for wSAA estimates of optimal values when problems can be solved exactly, characterizing how estimation uncertainty scales with covariate sample size. We then investigate practical scenarios with computational budget constraints, revealing a fundamental tradeoff between statistical accuracy and computational cost as sample sizes increase. Through central limit theorems for budget-constrained wSAA estimates, we precisely characterize this statistical-computational tradeoff. We also develop "over-optimizing" strategies for solving wSAA problems that ensure valid statistical inference. Extensive numerical experiments on both synthetic and real-world datasets validate our theoretical findings.

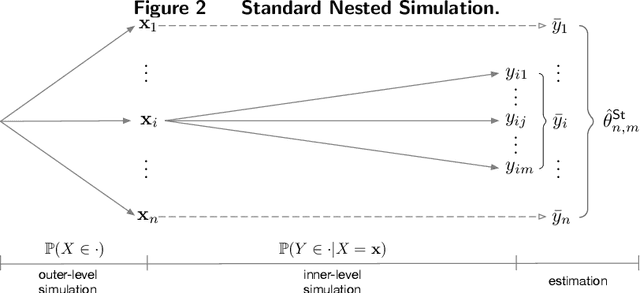

Smooth Nested Simulation: Bridging Cubic and Square Root Convergence Rates in High Dimensions

Jan 25, 2022

Nested simulation concerns estimating functionals of a conditional expectation via simulation. In this paper, we propose a new method based on kernel ridge regression to exploit the smoothness of the conditional expectation as a function of the multidimensional conditioning variable. Asymptotic analysis shows that the proposed method can effectively alleviate the curse of dimensionality on the convergence rate as the simulation budget increases, provided that the conditional expectation is sufficiently smooth. The smoothness bridges the gap between the cubic root convergence rate (that is, the optimal rate for the standard nested simulation) and the square root convergence rate (that is, the canonical rate for the standard Monte Carlo simulation). We demonstrate the performance of the proposed method via numerical examples from portfolio risk management and input uncertainty quantification.