Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeAlpha Mining and Enhancing via Warm Start Genetic Programming for Quantitative Investment

Dec 01, 2024

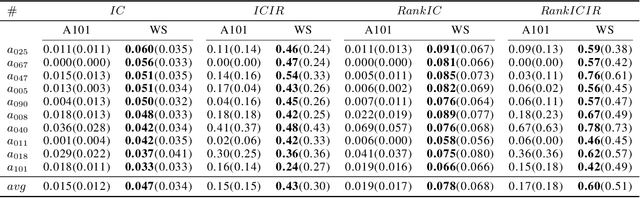

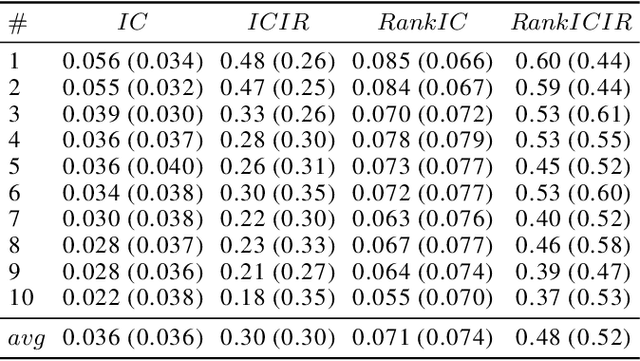

Traditional genetic programming (GP) often struggles in stock alpha factor discovery due to its vast search space, overwhelming computational burden, and sporadic effective alphas. We find that GP performs better when focusing on promising regions rather than random searching. This paper proposes a new GP framework with carefully chosen initialization and structural constraints to enhance search performance and improve the interpretability of the alpha factors. This approach is motivated by and mimics the alpha searching practice and aims to boost the efficiency of such a process. Analysis of 2020-2024 Chinese stock market data shows that our method yields superior out-of-sample prediction results and higher portfolio returns than the benchmark.