Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeMachine Learning on EPEX Order Books: Insights and Forecasts

Jun 27, 2019

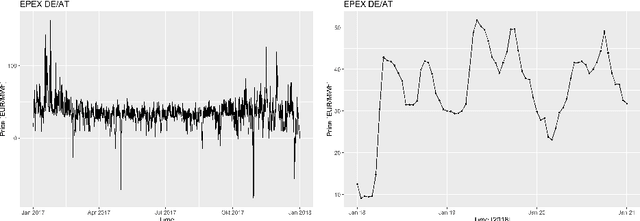

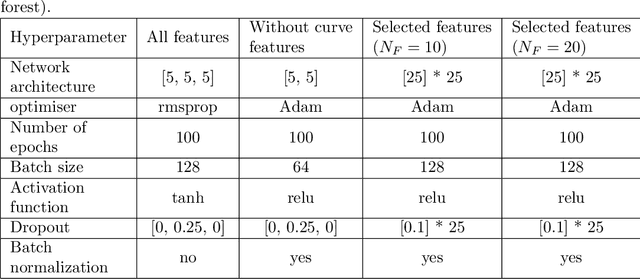

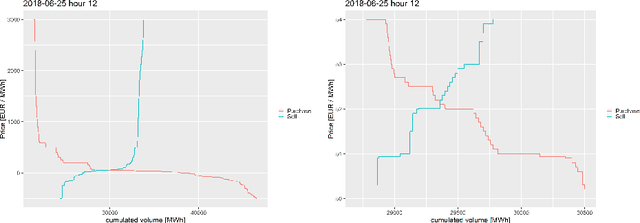

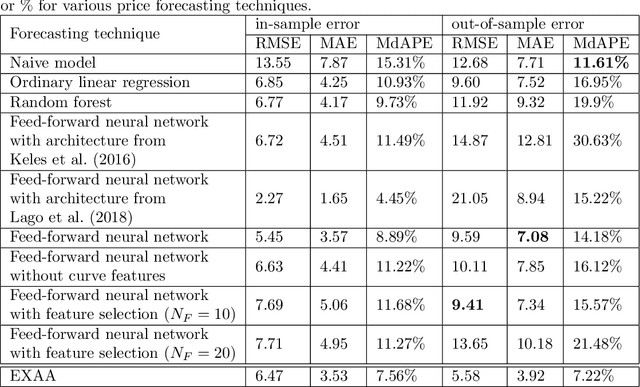

This paper employs machine learning algorithms to forecast German electricity spot market prices. The forecasts utilize in particular bid and ask order book data from the spot market but also fundamental market data like renewable infeed and expected demand. Appropriate feature extraction for the order book data is developed. Using cross-validation to optimise hyperparameters, neural networks and random forests are proposed and compared to statistical reference models. The machine learning models outperform traditional approaches.

* 14 pages, 5 figures

Via