Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeAdaptive learning for financial markets mixing model-based and model-free RL for volatility targeting

Apr 22, 2021

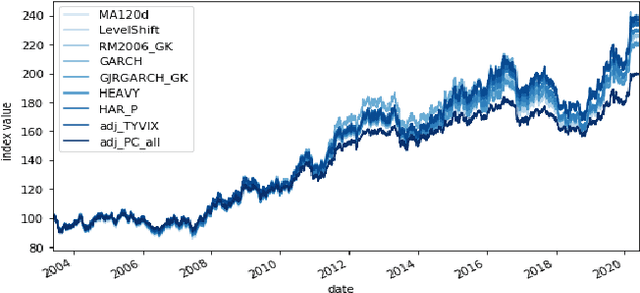

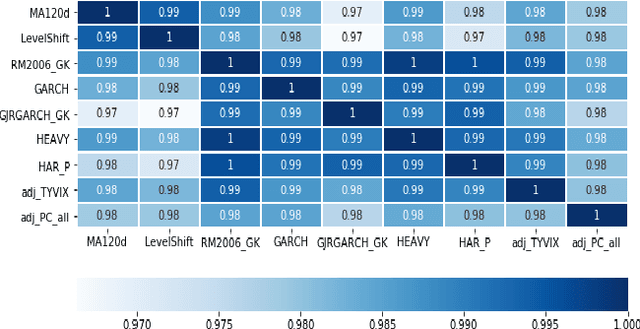

Model-Free Reinforcement Learning has achieved meaningful results in stable environments but, to this day, it remains problematic in regime changing environments like financial markets. In contrast, model-based RL is able to capture some fundamental and dynamical concepts of the environment but suffer from cognitive bias. In this work, we propose to combine the best of the two techniques by selecting various model-based approaches thanks to Model-Free Deep Reinforcement Learning. Using not only past performance and volatility, we include additional contextual information such as macro and risk appetite signals to account for implicit regime changes. We also adapt traditional RL methods to real-life situations by considering only past data for the training sets. Hence, we cannot use future information in our training data set as implied by K-fold cross validation. Building on traditional statistical methods, we use the traditional "walk-forward analysis", which is defined by successive training and testing based on expanding periods, to assert the robustness of the resulting agent. Finally, we present the concept of statistical difference's significance based on a two-tailed T-test, to highlight the ways in which our models differ from more traditional ones. Our experimental results show that our approach outperforms traditional financial baseline portfolio models such as the Markowitz model in almost all evaluation metrics commonly used in financial mathematics, namely net performance, Sharpe and Sortino ratios, maximum drawdown, maximum drawdown over volatility.