Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDeep reinforcement learning for portfolio management based on the empirical study of chinese stock market

Jan 10, 2021

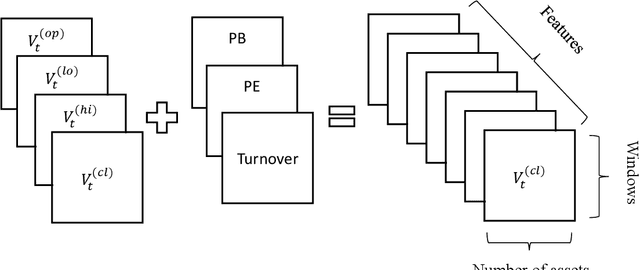

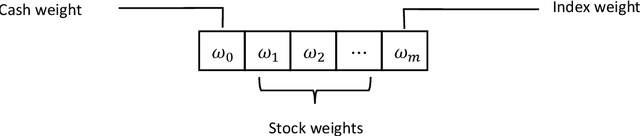

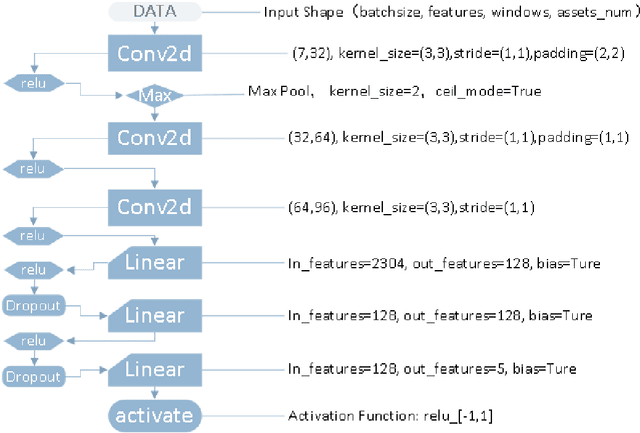

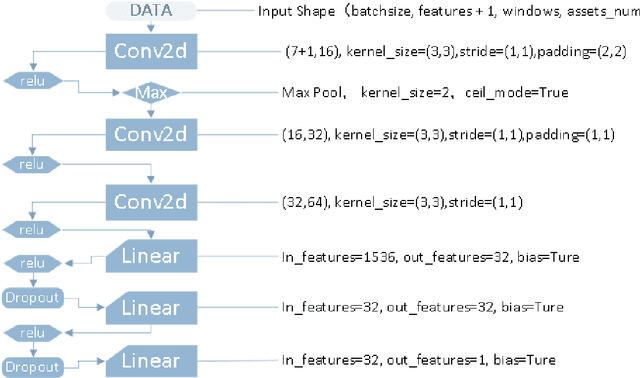

The objective of this paper is to verify that current cutting-edge artificial intelligence technology, deep reinforcement learning, can be applied to portfolio management. We improve on the existing Deep Reinforcement Learning Portfolio model and make many innovations. Unlike many previous studies on discrete trading signals in portfolio management, we make the agent to short in a continuous action space, design an arbitrage mechanism based on Arbitrage Pricing Theory,and redesign the activation function for acquiring action vectors, in addition, we redesign neural networks for reinforcement learning with reference to deep neural networks that process image data. In experiments, we use our model in several randomly selected portfolios which include CSI300 that represents the market's rate of return and the randomly selected constituents of CSI500. The experimental results show that no matter what stocks we select in our portfolios, we can almost get a higher return than the market itself. That is to say, we can defeat market by using deep reinforcement learning.