Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeTransformer for Times Series: an Application to the S&P500

Mar 04, 2024The transformer models have been extensively used with good results in a wide area of machine learning applications including Large Language Models and image generation. Here, we inquire on the applicability of this approach to financial time series. We first describe the dataset construction for two prototypical situations: a mean reverting synthetic Ornstein-Uhlenbeck process on one hand and real S&P500 data on the other hand. Then, we present in detail the proposed Transformer architecture and finally we discuss some encouraging results. For the synthetic data we predict rather accurately the next move, and for the S&P500 we get some interesting results related to quadratic variation and volatility prediction.

Onflow: an online portfolio allocation algorithm

Dec 08, 2023

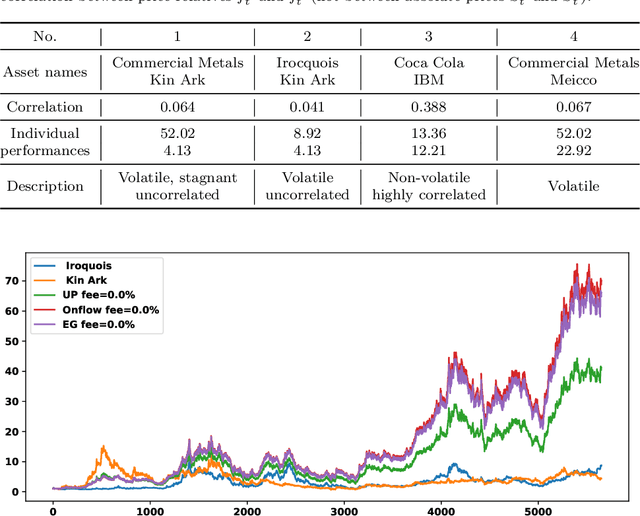

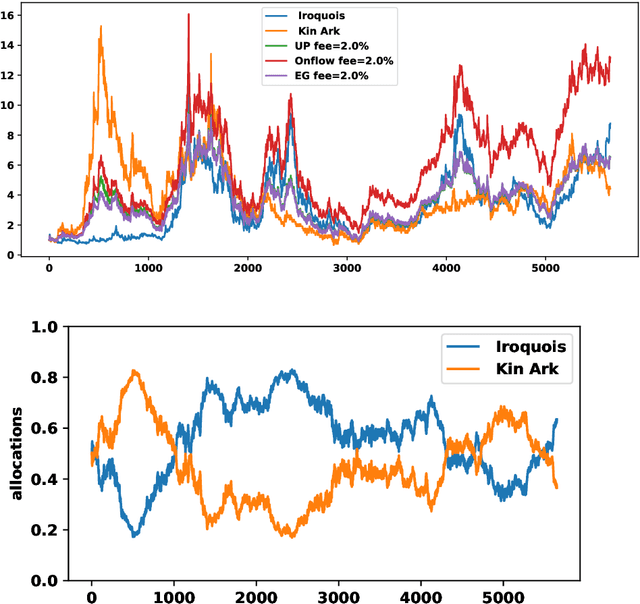

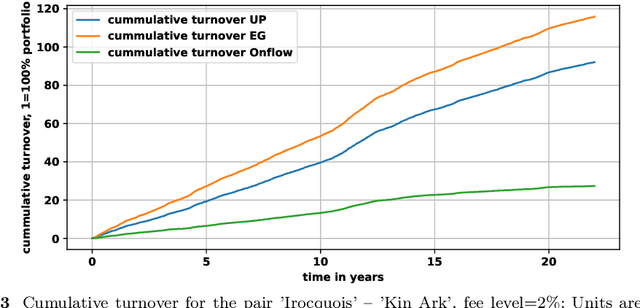

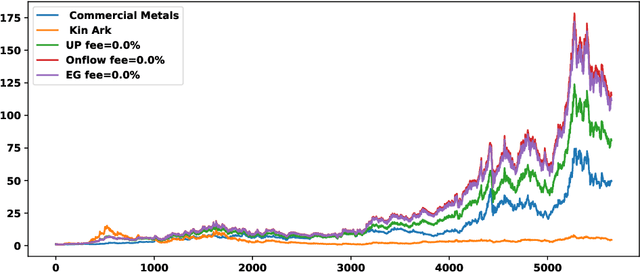

We introduce Onflow, a reinforcement learning technique that enables online optimization of portfolio allocation policies based on gradient flows. We devise dynamic allocations of an investment portfolio to maximize its expected log return while taking into account transaction fees. The portfolio allocation is parameterized through a softmax function, and at each time step, the gradient flow method leads to an ordinary differential equation whose solutions correspond to the updated allocations. This algorithm belongs to the large class of stochastic optimization procedures; we measure its efficiency by comparing our results to the mathematical theoretical values in a log-normal framework and to standard benchmarks from the 'old NYSE' dataset. For log-normal assets, the strategy learned by Onflow, with transaction costs at zero, mimics Markowitz's optimal portfolio and thus the best possible asset allocation strategy. Numerical experiments from the 'old NYSE' dataset show that Onflow leads to dynamic asset allocation strategies whose performances are: a) comparable to benchmark strategies such as Cover's Universal Portfolio or Helmbold et al. "multiplicative updates" approach when transaction costs are zero, and b) better than previous procedures when transaction costs are high. Onflow can even remain efficient in regimes where other dynamical allocation techniques do not work anymore. Therefore, as far as tested, Onflow appears to be a promising dynamic portfolio management strategy based on observed prices only and without any assumption on the laws of distributions of the underlying assets' returns. In particular it could avoid model risk when building a trading strategy.