Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeThe Application of Imperialist Competitive Algorithm for Fuzzy Random Portfolio Selection Problem

Feb 19, 2014

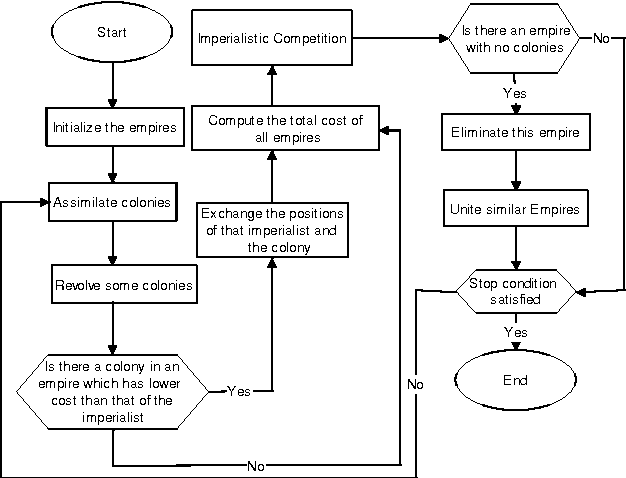

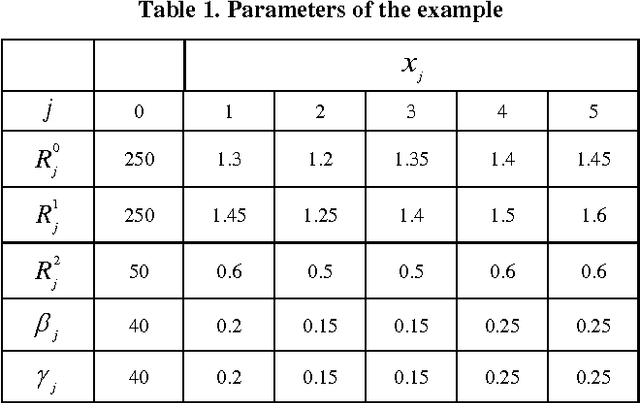

This paper presents an implementation of the Imperialist Competitive Algorithm (ICA) for solving the fuzzy random portfolio selection problem where the asset returns are represented by fuzzy random variables. Portfolio Optimization is an important research field in modern finance. By using the necessity-based model, fuzzy random variables reformulate to the linear programming and ICA will be designed to find the optimum solution. To show the efficiency of the proposed method, a numerical example illustrates the whole idea on implementation of ICA for fuzzy random portfolio selection problem.

* International Journal of Computer Applications 79(9):10-14,

October 2013

* 5 pages, 2 tables, Published with International Journal of Computer Applications (IJCA)

* 5 pages, 2 tables, Published with International Journal of Computer Applications (IJCA)

Via