Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeForecasting with an N-dimensional Langevin Equation and a Neural-Ordinary Differential Equation

May 12, 2024

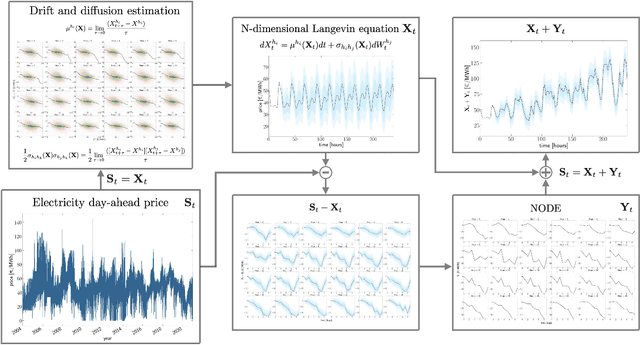

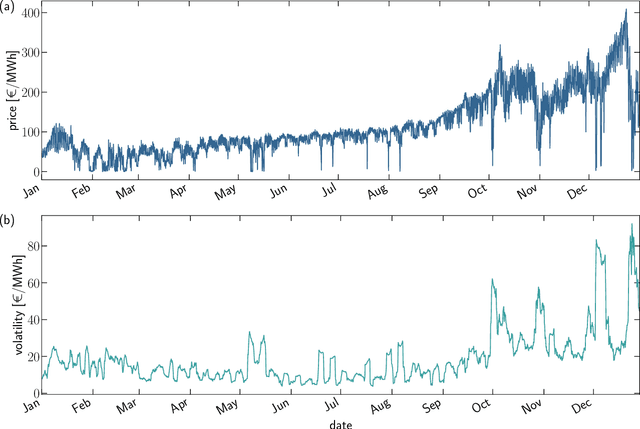

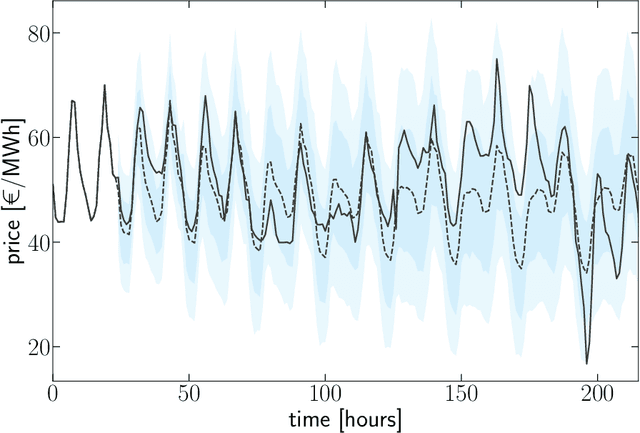

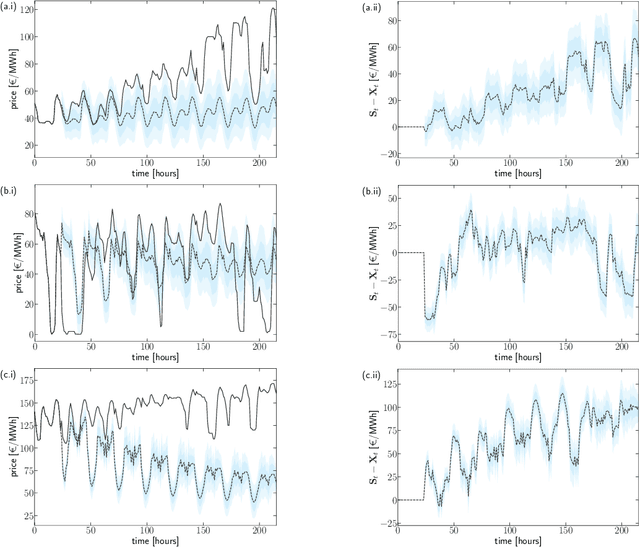

Accurate prediction of electricity day-ahead prices is essential in competitive electricity markets. Although stationary electricity-price forecasting techniques have received considerable attention, research on non-stationary methods is comparatively scarce, despite the common prevalence of non-stationary features in electricity markets. Specifically, existing non-stationary techniques will often aim to address individual non-stationary features in isolation, leaving aside the exploration of concurrent multiple non-stationary effects. Our overarching objective here is the formulation of a framework to systematically model and forecast non-stationary electricity-price time series, encompassing the broader scope of non-stationary behavior. For this purpose we develop a data-driven model that combines an N-dimensional Langevin equation (LE) with a neural-ordinary differential equation (NODE). The LE captures fine-grained details of the electricity-price behavior in stationary regimes but is inadequate for non-stationary conditions. To overcome this inherent limitation, we adopt a NODE approach to learn, and at the same time predict, the difference between the actual electricity-price time series and the simulated price trajectories generated by the LE. By learning this difference, the NODE reconstructs the non-stationary components of the time series that the LE is not able to capture. We exemplify the effectiveness of our framework using the Spanish electricity day-ahead market as a prototypical case study. Our findings reveal that the NODE nicely complements the LE, providing a comprehensive strategy to tackle both stationary and non-stationary electricity-price behavior. The framework's dependability and robustness is demonstrated through different non-stationary scenarios by comparing it against a range of basic naive methods.

* 26 pages, 7 figures

Physics-informed Bayesian inference of external potentials in classical density-functional theory

Sep 14, 2023

The swift progression of machine learning (ML) has not gone unnoticed in the realm of statistical mechanics. ML techniques have attracted attention by the classical density-functional theory (DFT) community, as they enable discovery of free-energy functionals to determine the equilibrium-density profile of a many-particle system. Within DFT, the external potential accounts for the interaction of the many-particle system with an external field, thus, affecting the density distribution. In this context, we introduce a statistical-learning framework to infer the external potential exerted on a many-particle system. We combine a Bayesian inference approach with the classical DFT apparatus to reconstruct the external potential, yielding a probabilistic description of the external potential functional form with inherent uncertainty quantification. Our framework is exemplified with a grand-canonical one-dimensional particle ensemble with excluded volume interactions in a confined geometry. The required training dataset is generated using a Monte Carlo (MC) simulation where the external potential is applied to the grand-canonical ensemble. The resulting particle coordinates from the MC simulation are fed into the learning framework to uncover the external potential. This eventually allows us to compute the equilibrium density profile of the system by using the tools of DFT. Our approach benchmarks the inferred density against the exact one calculated through the DFT formulation with the true external potential. The proposed Bayesian procedure accurately infers the external potential and the density profile. We also highlight the external-potential uncertainty quantification conditioned on the amount of available simulated data. The seemingly simple case study introduced in this work might serve as a prototype for studying a wide variety of applications, including adsorption and capillarity.