Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeEVaR-Optimal Arm Identification in Bandits

Oct 06, 2025

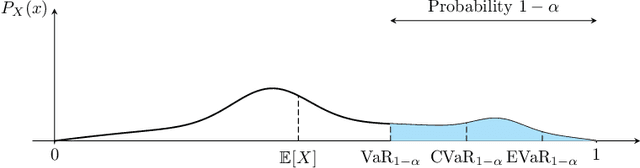

We study the fixed-confidence best arm identification (BAI) problem within the multi-armed bandit (MAB) framework under the Entropic Value-at-Risk (EVaR) criterion. Our analysis considers a nonparametric setting, allowing for general reward distributions bounded in [0,1]. This formulation addresses the critical need for risk-averse decision-making in high-stakes environments, such as finance, moving beyond simple expected value optimization. We propose a $\delta$-correct, Track-and-Stop based algorithm and derive a corresponding lower bound on the expected sample complexity, which we prove is asymptotically matched. The implementation of our algorithm and the characterization of the lower bound both require solving a complex convex optimization problem and a related, simpler non-convex one.

Identifying the Best Transition Law

Feb 17, 2025Motivated by recursive learning in Markov Decision Processes, this paper studies best-arm identification in bandit problems where each arm's reward is drawn from a multinomial distribution with a known support. We compare the performance { reached by strategies including notably LUCB without and with use of this knowledge. } In the first case, we use classical non-parametric approaches for the confidence intervals. In the second case, where a probability distribution is to be estimated, we first use classical deviation bounds (Hoeffding and Bernstein) on each dimension independently, and then the Empirical Likelihood method (EL-LUCB) on the joint probability vector. The effectiveness of these methods is demonstrated through simulations on scenarios with varying levels of structural complexity.