Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeA Deep Reinforcement Learning Framework for the Financial Portfolio Management Problem

Jul 16, 2017

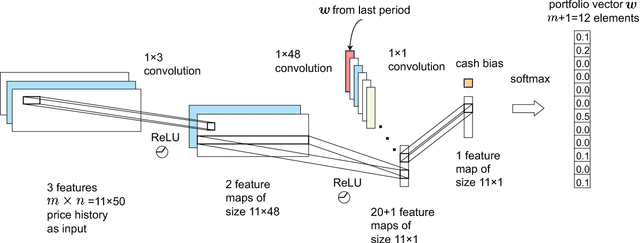

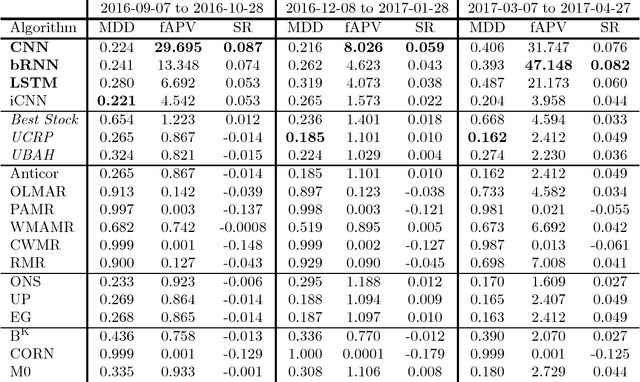

Financial portfolio management is the process of constant redistribution of a fund into different financial products. This paper presents a financial-model-free Reinforcement Learning framework to provide a deep machine learning solution to the portfolio management problem. The framework consists of the Ensemble of Identical Independent Evaluators (EIIE) topology, a Portfolio-Vector Memory (PVM), an Online Stochastic Batch Learning (OSBL) scheme, and a fully exploiting and explicit reward function. This framework is realized in three instants in this work with a Convolutional Neural Network (CNN), a basic Recurrent Neural Network (RNN), and a Long Short-Term Memory (LSTM). They are, along with a number of recently reviewed or published portfolio-selection strategies, examined in three back-test experiments with a trading period of 30 minutes in a cryptocurrency market. Cryptocurrencies are electronic and decentralized alternatives to government-issued money, with Bitcoin as the best-known example of a cryptocurrency. All three instances of the framework monopolize the top three positions in all experiments, outdistancing other compared trading algorithms. Although with a high commission rate of 0.25% in the backtests, the framework is able to achieve at least 4-fold returns in 50 days.

Cryptocurrency Portfolio Management with Deep Reinforcement Learning

May 11, 2017

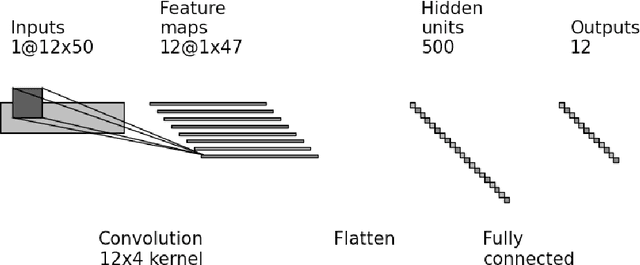

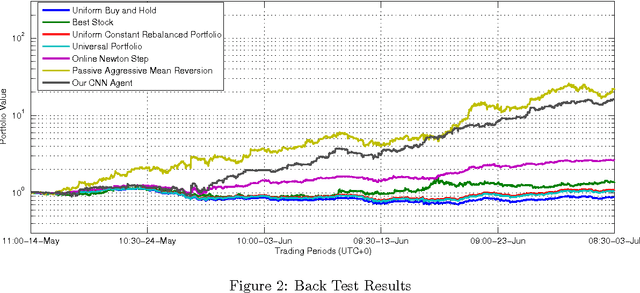

Portfolio management is the decision-making process of allocating an amount of fund into different financial investment products. Cryptocurrencies are electronic and decentralized alternatives to government-issued money, with Bitcoin as the best-known example of a cryptocurrency. This paper presents a model-less convolutional neural network with historic prices of a set of financial assets as its input, outputting portfolio weights of the set. The network is trained with 0.7 years' price data from a cryptocurrency exchange. The training is done in a reinforcement manner, maximizing the accumulative return, which is regarded as the reward function of the network. Backtest trading experiments with trading period of 30 minutes is conducted in the same market, achieving 10-fold returns in 1.8 months' periods. Some recently published portfolio selection strategies are also used to perform the same back-tests, whose results are compared with the neural network. The network is not limited to cryptocurrency, but can be applied to any other financial markets.