Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeA new multilayer network construction via Tensor learning

Apr 11, 2020

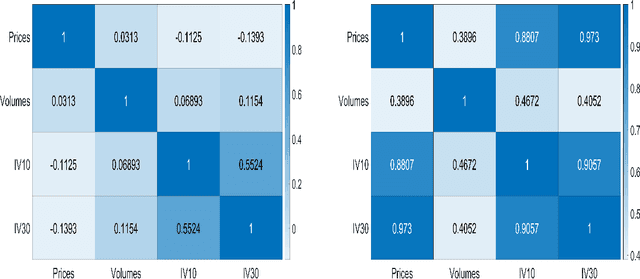

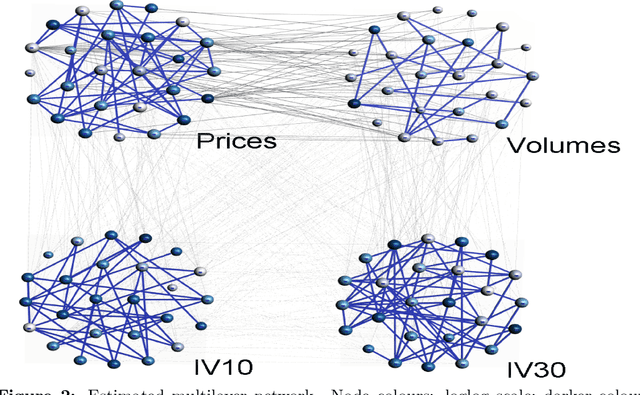

Multilayer networks proved to be suitable in extracting and providing dependency information of different complex systems. The construction of these networks is difficult and is mostly done with a static approach, neglecting time delayed interdependences. Tensors are objects that naturally represent multilayer networks and in this paper, we propose a new methodology based on Tucker tensor autoregression in order to build a multilayer network directly from data. This methodology captures within and between connections across layers and makes use of a filtering procedure to extract relevant information and improve visualization. We show the application of this methodology to different stationary fractionally differenced financial data. We argue that our result is useful to understand the dependencies across three different aspects of financial risk, namely market risk, liquidity risk, and volatility risk. Indeed, we show how the resulting visualization is a useful tool for risk managers depicting dependency asymmetries between different risk factors and accounting for delayed cross dependencies. The constructed multilayer network shows a strong interconnection between the volumes and prices layers across all the stocks considered while a lower number of interconnections between the uncertainty measures is identified.

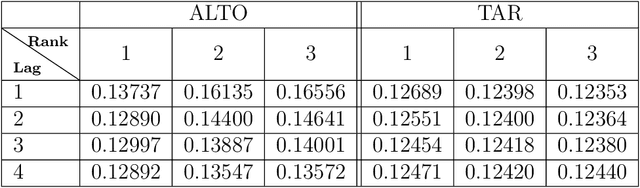

Predicting Multidimensional Data via Tensor Learning

Feb 11, 2020

The analysis of multidimensional data is becoming a more and more relevant topic in statistical and machine learning research. Given their complexity, such data objects are usually reshaped into matrices or vectors and then analysed. However, this methodology presents several drawbacks. First of all, it destroys the intrinsic interconnections among datapoints in the multidimensional space and, secondly, the number of parameters to be estimated in a model increases exponentially. We develop a model that overcomes such drawbacks. In particular, we proposed a parsimonious tensor regression based model that retains the intrinsic multidimensional structure of the dataset. Tucker structure is employed to achieve parsimony and a shrinkage penalization is introduced to deal with over-fitting and collinearity. An Alternating Least Squares (ALS) algorithm is developed to estimate the model parameters. A simulation exercise is produced to validate the model and its robustness. Finally, an empirical application to Foursquares spatio-temporal dataset and macroeconomic time series is also performed. Overall, the proposed model is able to outperform existing models present in forecasting literature.