Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeA Comparative Study of Rule-Based and Data-Driven Approaches in Industrial Monitoring

Sep 19, 2025Industrial monitoring systems, especially when deployed in Industry 4.0 environments, are experiencing a shift in paradigm from traditional rule-based architectures to data-driven approaches leveraging machine learning and artificial intelligence. This study presents a comparison between these two methodologies, analyzing their respective strengths, limitations, and application scenarios, and proposes a basic framework to evaluate their key properties. Rule-based systems offer high interpretability, deterministic behavior, and ease of implementation in stable environments, making them ideal for regulated industries and safety-critical applications. However, they face challenges with scalability, adaptability, and performance in complex or evolving contexts. Conversely, data-driven systems excel in detecting hidden anomalies, enabling predictive maintenance and dynamic adaptation to new conditions. Despite their high accuracy, these models face challenges related to data availability, explainability, and integration complexity. The paper suggests hybrid solutions as a possible promising direction, combining the transparency of rule-based logic with the analytical power of machine learning. Our hypothesis is that the future of industrial monitoring lies in intelligent, synergic systems that leverage both expert knowledge and data-driven insights. This dual approach enhances resilience, operational efficiency, and trust, paving the way for smarter and more flexible industrial environments.

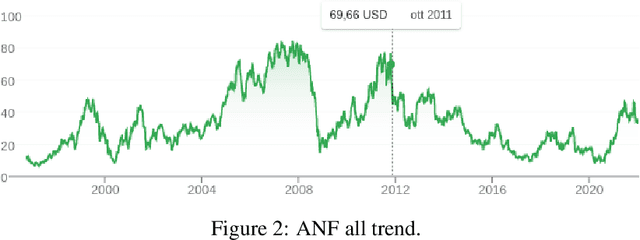

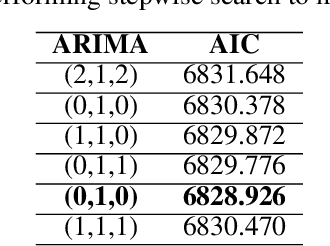

A Stock Trading System for a Medium Volatile Asset using Multi Layer Perceptron

Jan 17, 2022

Stock market forecasting is a lucrative field of interest with promising profits but not without its difficulties and for some people could be even causes of failure. Financial markets by their nature are complex, non-linear and chaotic, which implies that accurately predicting the prices of assets that are part of it becomes very complicated. In this paper we propose a stock trading system having as main core the feed-forward deep neural networks (DNN) to predict the price for the next 30 days of open market, of the shares issued by Abercrombie & Fitch Co. (ANF) in the stock market of the New York Stock Exchange (NYSE). The system we have elaborated calculates the most effective technical indicator, applying it to the predictions computed by the DNNs, for generating trades. The results showed an increase in values such as Expectancy Ratio of 2.112% of profitable trades with Sharpe, Sortino, and Calmar Ratios of 2.194, 3.340, and 12.403 respectively. As a verification, we adopted a backtracking simulation module in our system, which maps trades to actual test data consisting of the last 30 days of open market on the ANF asset. Overall, the results were promising bringing a total profit factor of 3.2% in just one month from a very modest budget of $100. This was possible because the system reduced the number of trades by choosing the most effective and efficient trades, saving on commissions and slippage costs.

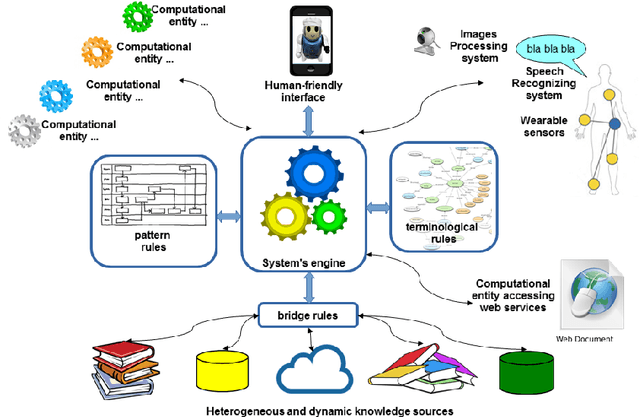

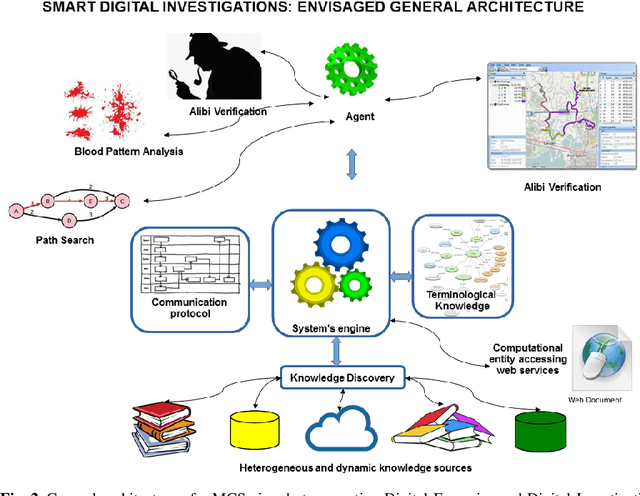

Multi-Context Systems: Dynamics and Evolution (Pre-Print of "Multi-context systems in dynamic environments")

Jun 12, 2021

Multi-Context Systems (MCS) model in Computational Logic distributed systems composed of heterogeneous sources, or "contexts", interacting via special rules called "bridge rules". In this paper, we consider how to enhance flexibility and generality in bridge-rules definition and application. In particular, we introduce and discuss some formal extensions of MCSs useful for a practical use in dynamic environments, and we try to provide guidelines for implementations

* 35 pages 2 figures