Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeRandomized Signature Methods in Optimal Portfolio Selection

Dec 27, 2023We present convincing empirical results on the application of Randomized Signature Methods for non-linear, non-parametric drift estimation for a multi-variate financial market. Even though drift estimation is notoriously ill defined due to small signal to noise ratio, one can still try to learn optimal non-linear maps from data to future returns for the purposes of portfolio optimization. Randomized Signatures, in contrast to classical signatures, allow for high dimensional market dimension and provide features on the same scale. We do not contribute to the theory of Randomized Signatures here, but rather present our empirical findings on portfolio selection in real world settings including real market data and transaction costs.

Applications of Signature Methods to Market Anomaly Detection

Feb 08, 2022

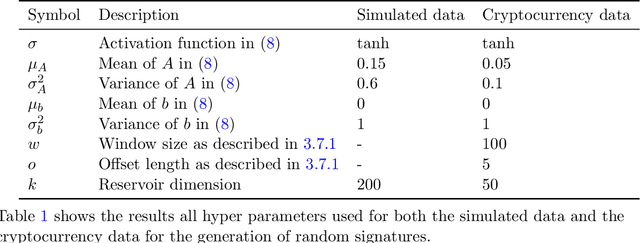

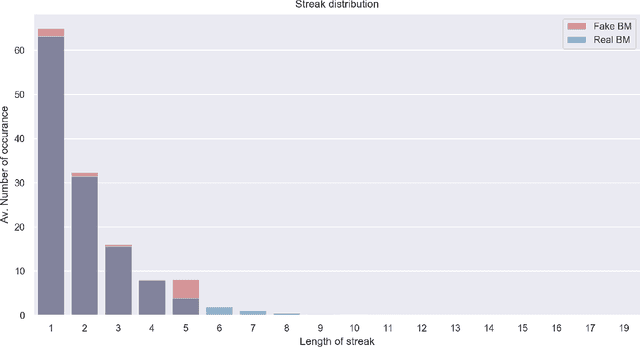

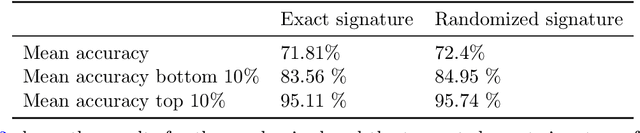

Anomaly detection is the process of identifying abnormal instances or events in data sets which deviate from the norm significantly. In this study, we propose a signatures based machine learning algorithm to detect rare or unexpected items in a given data set of time series type. We present applications of signature or randomized signature as feature extractors for anomaly detection algorithms; additionally we provide an easy, representation theoretic justification for the construction of randomized signatures. Our first application is based on synthetic data and aims at distinguishing between real and fake trajectories of stock prices, which are indistinguishable by visual inspection. We also show a real life application by using transaction data from the cryptocurrency market. In this case, we are able to identify pump and dump attempts organized on social networks with F1 scores up to 88% by means of our unsupervised learning algorithm, thus achieving results that are close to the state-of-the-art in the field based on supervised learning.