Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeOn Feature Reduction using Deep Learning for Trend Prediction in Finance

Apr 11, 2017

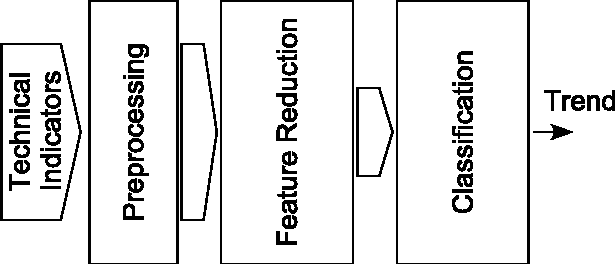

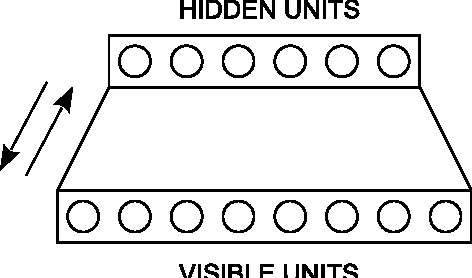

One of the major advantages in using Deep Learning for Finance is to embed a large collection of information into investment decisions. A way to do that is by means of compression, that lead us to consider a smaller feature space. Several studies are proving that non-linear feature reduction performed by Deep Learning tools is effective in price trend prediction. The focus has been put mainly on Restricted Boltzmann Machines (RBM) and on output obtained by them. Few attention has been payed to Auto-Encoders (AE) as an alternative means to perform a feature reduction. In this paper we investigate the application of both RBM and AE in more general terms, attempting to outline how architectural and input space characteristics can affect the quality of prediction.