Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeOptimal anytime regret with two experts

Feb 20, 2020

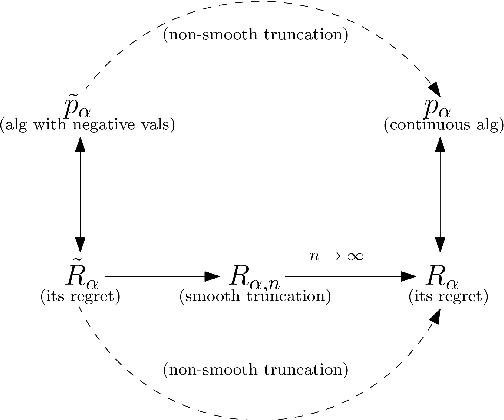

The multiplicative weights method is an algorithm for the problem of prediction with expert advice. It achieves the minimax regret asymptotically if the number of experts is large, and the time horizon is known in advance. Optimal algorithms are also known if there are exactly two or three experts, and the time horizon is known in advance. In the anytime setting, where the time horizon is not known in advance, algorithms can be obtained by the doubling trick, but they are not optimal, let alone practical. No minimax optimal algorithm was previously known in the anytime setting, regardless of the number of experts. We design the first minimax optimal algorithm for minimizing regret in the anytime setting. We consider the case of two experts, and prove that the optimal regret is $\gamma \sqrt{t} / 2$ at all time steps $t$, where $\gamma$ is a natural constant that arose 35 years ago in studying fundamental properties of Brownian motion. The algorithm is designed by considering a continuous analogue, which is solved using ideas from stochastic calculus.