Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeA Second Order Cumulant Spectrum Based Test for Strict Stationarity

Jan 20, 2018

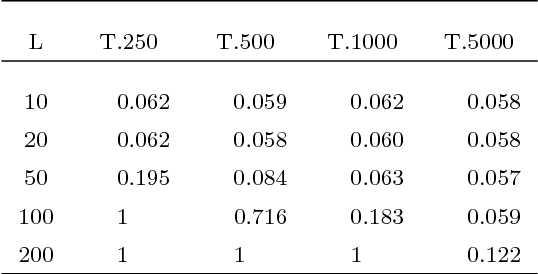

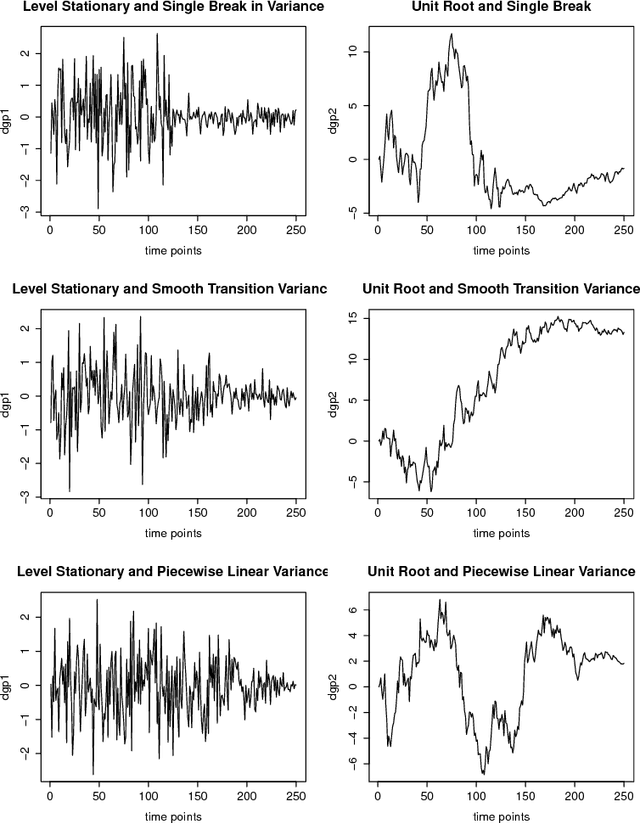

This article develops a statistical test for the null hypothesis of strict stationarity of a discrete time stochastic process. When the null hypothesis is true, the second order cumulant spectrum is zero at all the discrete Fourier frequency pairs present in the principal domain of the cumulant spectrum. The test uses a frame (window) averaged sample estimate of the second order cumulant spectrum to build a test statistic that has an asymptotic complex standard normal distribution. We derive the test statistic, study the size and power properties of the test, and demonstrate its implementation with intraday stock market return data. The test has conservative size properties and good power to detect varying variance and unit root in the presence of varying variance.