Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeAxial-LOB: High-Frequency Trading with Axial Attention

Dec 04, 2022Previous attempts to predict stock price from limit order book (LOB) data are mostly based on deep convolutional neural networks. Although convolutions offer efficiency by restricting their operations to local interactions, it is at the cost of potentially missing out on the detection of long-range dependencies. Recent studies address this problem by employing additional recurrent or attention layers that increase computational complexity. In this work, we propose Axial-LOB, a novel fully-attentional deep learning architecture for predicting price movements of stocks from LOB data. By utilizing gated position-sensitive axial attention layers our architecture is able to construct feature maps that incorporate global interactions, while significantly reducing the size of the parameter space. Unlike previous works, Axial-LOB does not rely on hand-crafted convolutional kernels and hence has stable performance under input permutations and the capacity to incorporate additional LOB features. The effectiveness of Axial-LOB is demonstrated on a large benchmark dataset, containing time series representations of millions of high-frequency trading events, where our model establishes a new state of the art, achieving an excellent directional classification performance at all tested prediction horizons.

A Meta-Method for Portfolio Management Using Machine Learning for Adaptive Strategy Selection

Nov 10, 2021

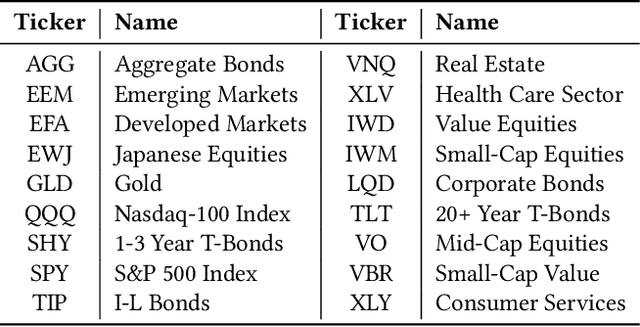

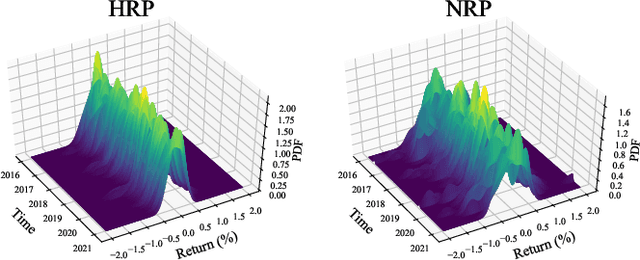

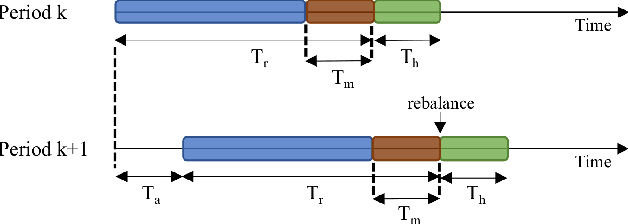

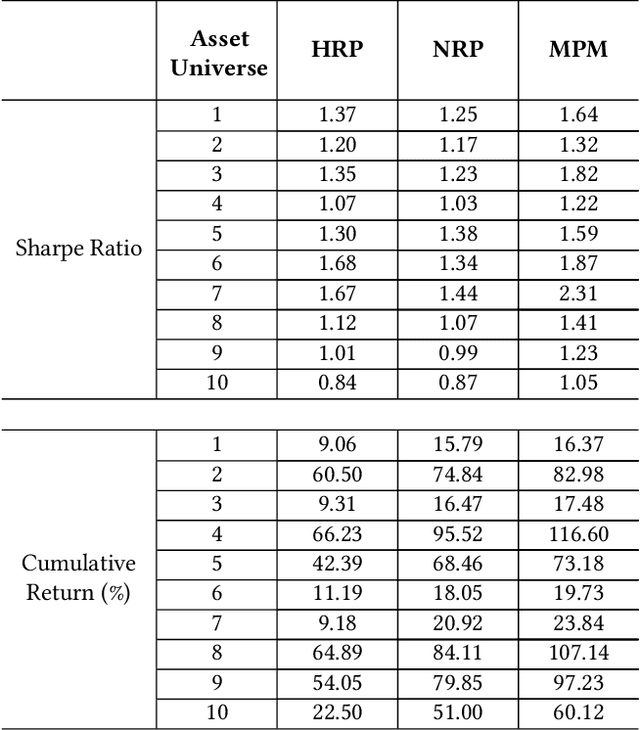

This work proposes a novel portfolio management technique, the Meta Portfolio Method (MPM), inspired by the successes of meta approaches in the field of bioinformatics and elsewhere. The MPM uses XGBoost to learn how to switch between two risk-based portfolio allocation strategies, the Hierarchical Risk Parity (HRP) and more classical Na\"ive Risk Parity (NRP). It is demonstrated that the MPM is able to successfully take advantage of the best characteristics of each strategy (the NRP's fast growth during market uptrends, and the HRP's protection against drawdowns during market turmoil). As a result, the MPM is shown to possess an excellent out-of-sample risk-reward profile, as measured by the Sharpe ratio, and in addition offers a high degree of interpretability of its asset allocation decisions.