Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeHierarchical Representations for Evolving Acyclic Vector Autoregressions (HEAVe)

May 19, 2025Causal networks offer an intuitive framework to understand influence structures within time series systems. However, the presence of cycles can obscure dynamic relationships and hinder hierarchical analysis. These networks are typically identified through multivariate predictive modelling, but enforcing acyclic constraints significantly increases computational and analytical complexity. Despite recent advances, there remains a lack of simple, flexible approaches that are easily tailorable to specific problem instances. We propose an evolutionary approach to fitting acyclic vector autoregressive processes and introduces a novel hierarchical representation that directly models structural elements within a time series system. On simulated datasets, our model retains most of the predictive accuracy of unconstrained models and outperforms permutation-based alternatives. When applied to a dataset of 100 cryptocurrency return series, our method generates acyclic causal networks capturing key structural properties of the unconstrained model. The acyclic networks are approximately sub-graphs of the unconstrained networks, and most of the removed links originate from low-influence nodes. Given the high levels of feature preservation, we conclude that this cryptocurrency price system functions largely hierarchically. Our findings demonstrate a flexible, intuitive approach for identifying hierarchical causal networks in time series systems, with broad applications to fields like econometrics and social network analysis.

A probabilistic forecast methodology for volatile electricity prices in the Australian National Electricity Market

Nov 13, 2023

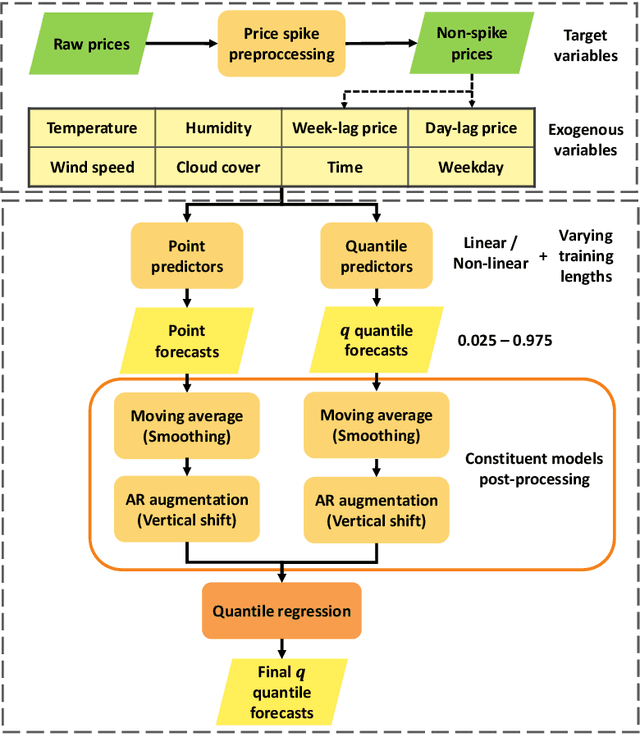

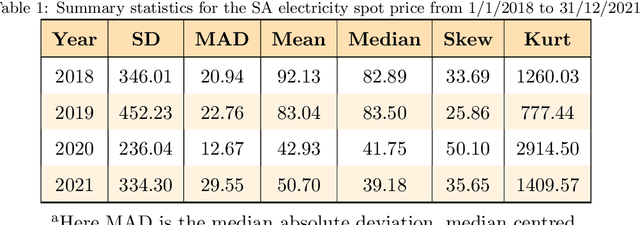

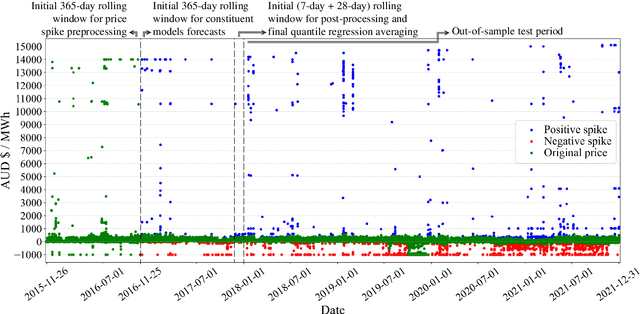

The South Australia region of the Australian National Electricity Market (NEM) displays some of the highest levels of price volatility observed in modern electricity markets. This paper outlines an approach to probabilistic forecasting under these extreme conditions, including spike filtration and several post-processing steps. We propose using quantile regression as an ensemble tool for probabilistic forecasting, with our combined forecasts achieving superior results compared to all constituent models. Within our ensemble framework, we demonstrate that averaging models with varying training length periods leads to a more adaptive model and increased prediction accuracy. The applicability of the final model is evaluated by comparing our median forecasts with the point forecasts available from the Australian NEM operator, with our model outperforming these NEM forecasts by a significant margin.