Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeRTB Formulation Using Point Process

Aug 17, 2023

We propose a general stochastic framework for modelling repeated auctions in the Real Time Bidding (RTB) ecosystem using point processes. The flexibility of the framework allows a variety of auction scenarios including configuration of information provided to player, determination of auction winner and quantification of utility gained from each auctions. We propose theoretical results on how this formulation of process can be approximated to a Poisson point process, which enables the analyzer to take advantage of well-established properties. Under this framework, we specify the player's optimal strategy under various scenarios. We also emphasize that it is critical to consider the joint distribution of utility and market condition instead of estimating the marginal distributions independently.

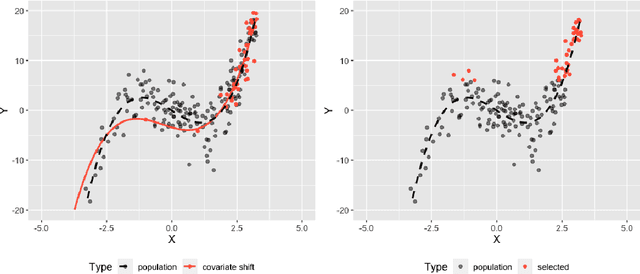

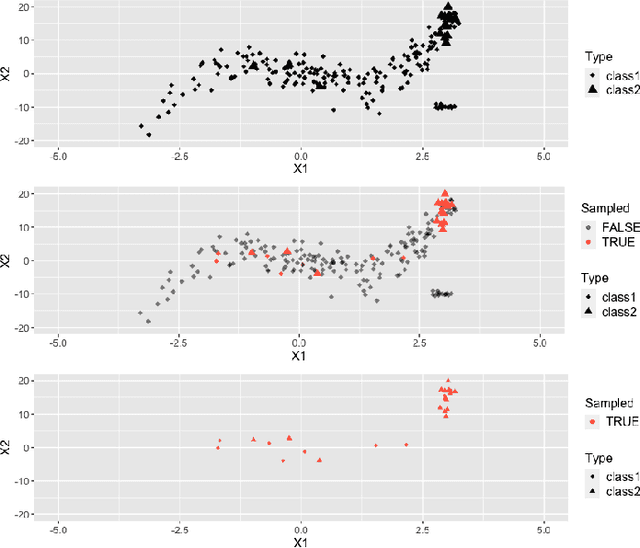

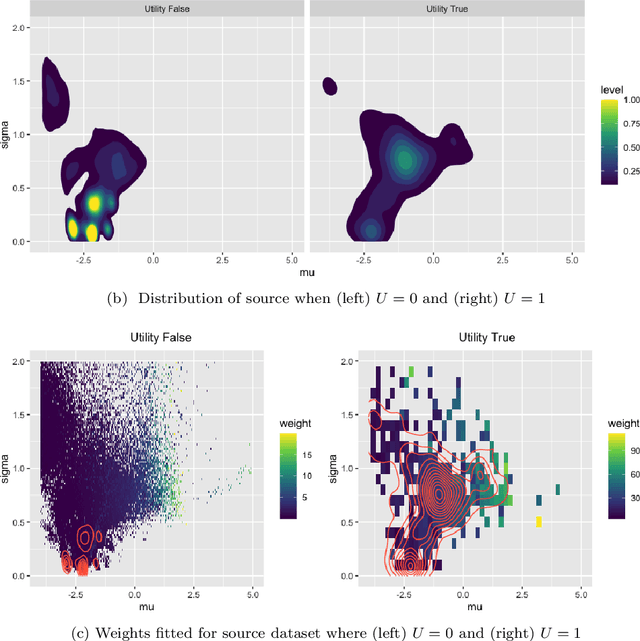

Addressing Distribution Shift in RTB Markets via Exponential Tilting

Aug 14, 2023

Distribution shift in machine learning models can be a primary cause of performance degradation. This paper delves into the characteristics of these shifts, primarily motivated by Real-Time Bidding (RTB) market models. We emphasize the challenges posed by class imbalance and sample selection bias, both potent instigators of distribution shifts. This paper introduces the Exponential Tilt Reweighting Alignment (ExTRA) algorithm, as proposed by Marty et al. (2023), to address distribution shifts in data. The ExTRA method is designed to determine the importance weights on the source data, aiming to minimize the KL divergence between the weighted source and target datasets. A notable advantage of this method is its ability to operate using labeled source data and unlabeled target data. Through simulated real-world data, we investigate the nature of distribution shift and evaluate the applicacy of the proposed model.