Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeEUR/USD Exchange Rate Forecasting incorporating Text Mining Based on Pre-trained Language Models and Deep Learning Methods

Nov 12, 2024

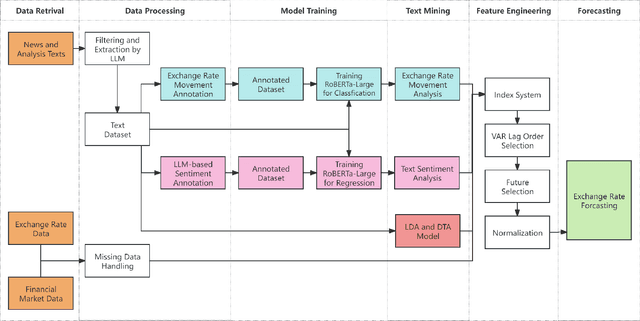

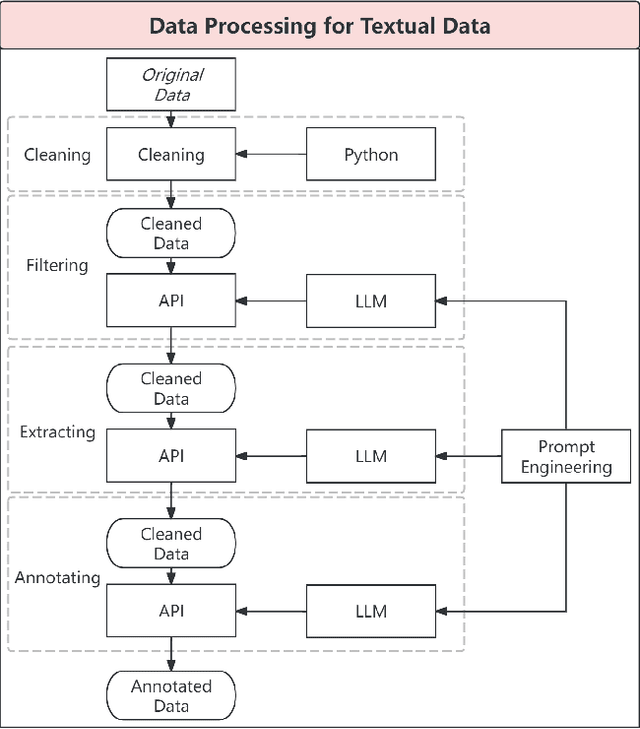

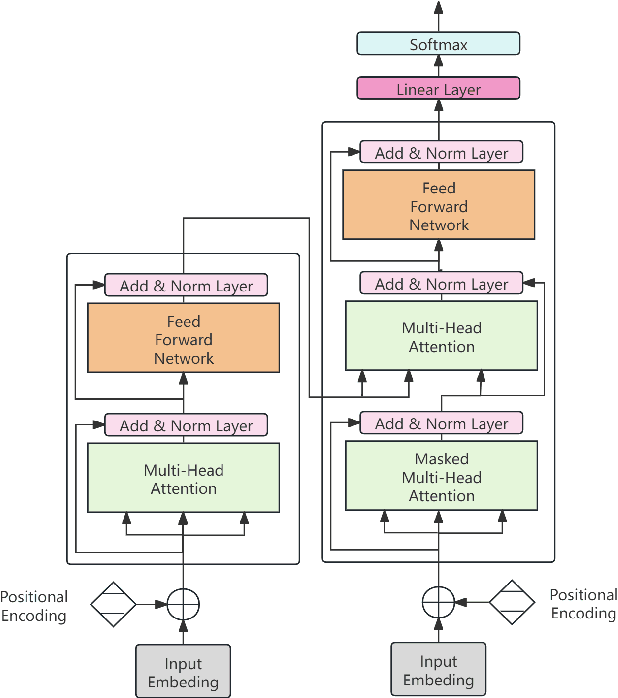

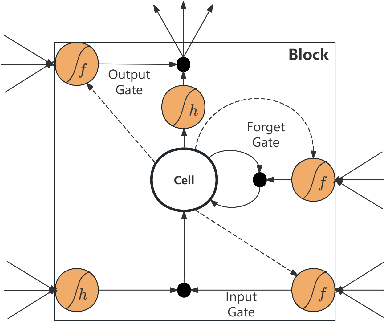

This study introduces a novel approach for EUR/USD exchange rate forecasting that integrates deep learning, textual analysis, and particle swarm optimization (PSO). By incorporating online news and analysis texts as qualitative data, the proposed PSO-LSTM model demonstrates superior performance compared to traditional econometric and machine learning models. The research employs advanced text mining techniques, including sentiment analysis using the RoBERTa-Large model and topic modeling with LDA. Empirical findings underscore the significant advantage of incorporating textual data, with the PSO-LSTM model outperforming benchmark models such as SVM, SVR, ARIMA, and GARCH. Ablation experiments reveal the contribution of each textual data category to the overall forecasting performance. The study highlights the transformative potential of artificial intelligence in finance and paves the way for future research in real-time forecasting and the integration of alternative data sources.