Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeBeyond Surrogate Modeling: Learning the Local Volatility Via Shape Constraints

Dec 20, 2022We explore the abilities of two machine learning approaches for no-arbitrage interpolation of European vanilla option prices, which jointly yield the corresponding local volatility surface: a finite dimensional Gaussian process (GP) regression approach under no-arbitrage constraints based on prices, and a neural net (NN) approach with penalization of arbitrages based on implied volatilities. We demonstrate the performance of these approaches relative to the SSVI industry standard. The GP approach is proven arbitrage-free, whereas arbitrages are only penalized under the SSVI and NN approaches. The GP approach obtains the best out-of-sample calibration error and provides uncertainty quantification.The NN approach yields a smoother local volatility and a better backtesting performance, as its training criterion incorporates a local volatility regularization term.

Rating transitions forecasting: a filtering approach

Sep 22, 2021

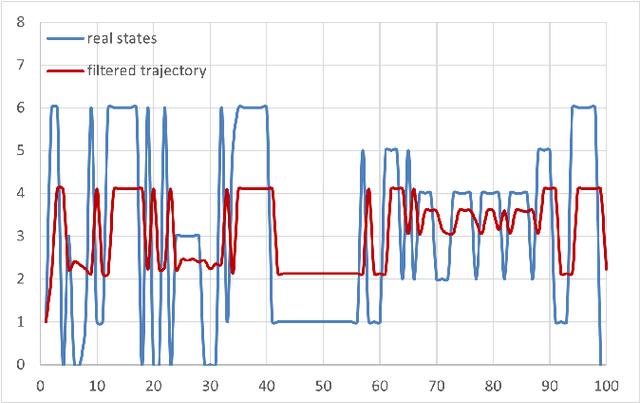

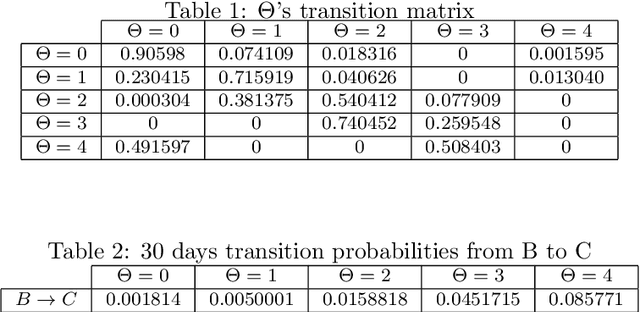

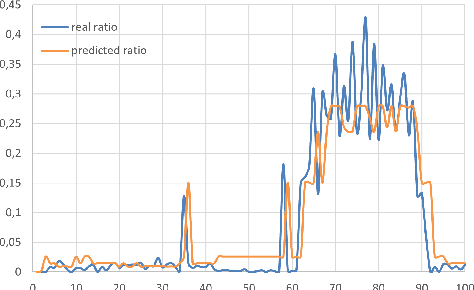

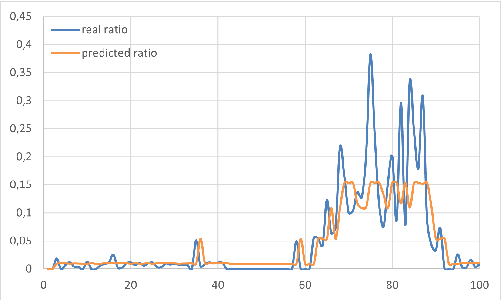

Analyzing the effect of business cycle on rating transitions has been a subject of great interest these last fifteen years, particularly due to the increasing pressure coming from regulators for stress testing. In this paper, we consider that the dynamics of rating migrations is governed by an unobserved latent factor. Under a point process filtering framework, we explain how the current state of the hidden factor can be efficiently inferred from observations of rating histories. We then adapt the classical Baum-Welsh algorithm to our setting and show how to estimate the latent factor parameters. Once calibrated, we may reveal and detect economic changes affecting the dynamics of rating migration, in real-time. To this end we adapt a filtering formula which can then be used for predicting future transition probabilities according to economic regimes without using any external covariates. We propose two filtering frameworks: a discrete and a continuous version. We demonstrate and compare the efficiency of both approaches on fictive data and on a corporate credit rating database. The methods could also be applied to retail credit loans.