Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeBayesian Neural Networks with Monte Carlo Dropout for Probabilistic Electricity Price Forecasting

Nov 12, 2025

Accurate electricity price forecasting is critical for strategic decision-making in deregulated electricity markets, where volatility stems from complex supply-demand dynamics and external factors. Traditional point forecasts often fail to capture inherent uncertainties, limiting their utility for risk management. This work presents a framework for probabilistic electricity price forecasting using Bayesian neural networks (BNNs) with Monte Carlo (MC) dropout, training separate models for each hour of the day to capture diurnal patterns. A critical assessment and comparison with the benchmark model, namely: generalized autoregressive conditional heteroskedasticity with exogenous variable (GARCHX) model and the LASSO estimated auto-regressive model (LEAR), highlights that the proposed model outperforms the benchmark models in terms of point prediction and intervals. This work serves as a reference for leveraging probabilistic neural models in energy market predictions.

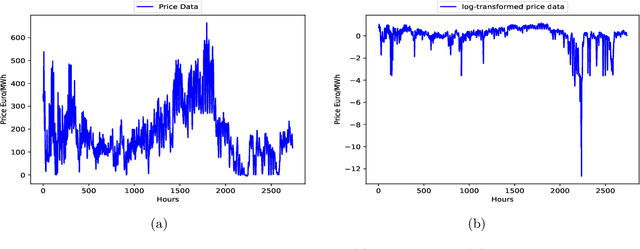

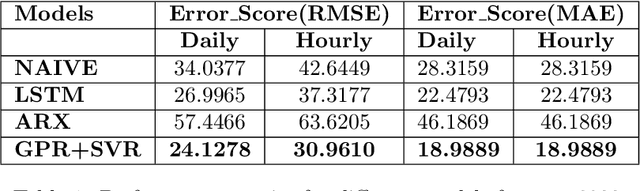

Electricity Price Prediction Using Multi-Kernel Gaussian Process Regression combined with Kernel-Based Support Vector Regression

Nov 28, 2024

This paper presents a new hybrid model for predicting German electricity prices. The algorithm is based on combining Gaussian Process Regression (GPR) and Support Vector Regression (SVR). While GPR is a competent model for learning the stochastic pattern within the data and interpolation, its performance for out-of-sample data is not very promising. By choosing a suitable data-dependent covariance function, we can enhance the performance of GPR for the tested German hourly power prices. However, since the out-of-sample prediction depends on the training data, the prediction is vulnerable to noise and outliers. To overcome this issue, a separate prediction is made using SVR, which applies margin-based optimization, having an advantage in dealing with non-linear processes and outliers, since only certain necessary points (support vectors) in the training data are responsible for regression. Both individual predictions are later combined using the performance-based weight assignment method. A test on historic German power prices shows that this approach outperforms its chosen benchmarks such as the autoregressive exogenous model, the naive approach, as well as the long short-term memory approach of prediction.