Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeWhere does the Stimulus go? Deep Generative Model for Commercial Banking Deposits

Paper and Code

Jan 22, 2021

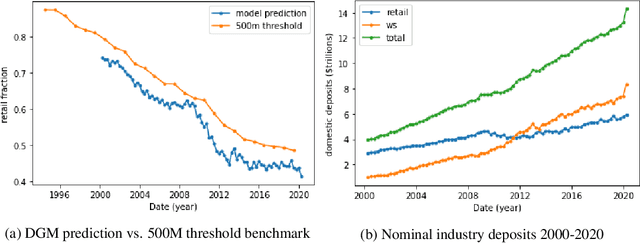

This paper examines deposits of individuals ("retail") and large companies ("wholesale") in the U.S. banking industry, and how these deposit types are impacted by macroeconomic factors, such as quantitative easing (QE). Actual data for deposits by holder are unavailable. We use a dataset on banks' financial information and probabilistic generative model to predict industry retail-wholesale deposit split from 2000 to 2020. Our model assumes account balances arise from separate retail and wholesale lognormal distributions and fit parameters of distributions by minimizing error between actual bank metrics and simulated metrics using the model's generative process. We use time-series regression to forward predict retail-wholesale deposits as function of loans, retail loans, and reserve balances at Fed banks. We find increase in reserves (representing QE) increases wholesale but not retail deposits, and increase in loans increase both wholesale and retail deposits evenly. The result shows that QE following the 2008 financial crisis benefited large companies more than average individuals, a relevant finding for economic decision making. In addition, this work benefits bank management strategy by providing forecasting capability for retail-wholesale deposits.