Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeWarped Input Gaussian Processes for Time Series Forecasting

Paper and Code

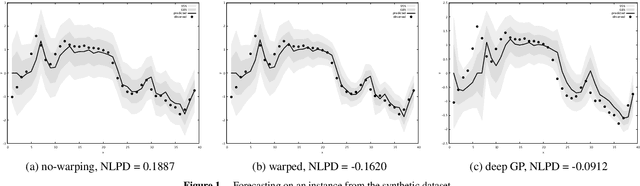

We introduce a Gaussian process-based model for handling of non-stationarity. The warping is achieved non-parametrically, through imposing a prior on the relative change of distance between subsequent observation inputs. The model allows the use of general gradient optimization algorithms for training and incurs only a small computational overhead on training and prediction. The model finds its applications in forecasting in non-stationary time series with either gradually varying volatility, presence of change points, or a combination thereof. We evaluate the model on synthetic and real-world time series data comparing against both baseline and known state-of-the-art approaches and show that the model exhibits state-of-the-art forecasting performance at a lower implementation and computation cost.