Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeUnderstanding algorithmic collusion with experience replay

Paper and Code

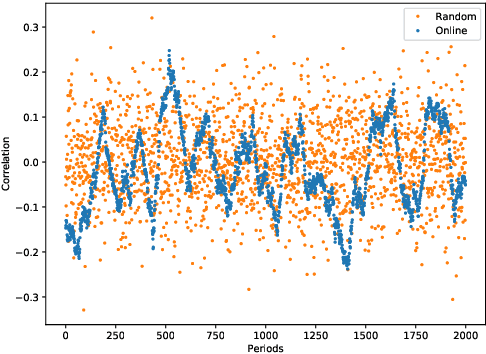

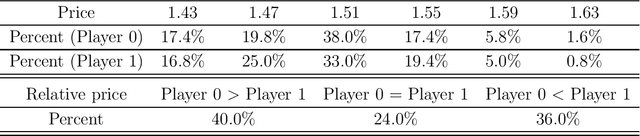

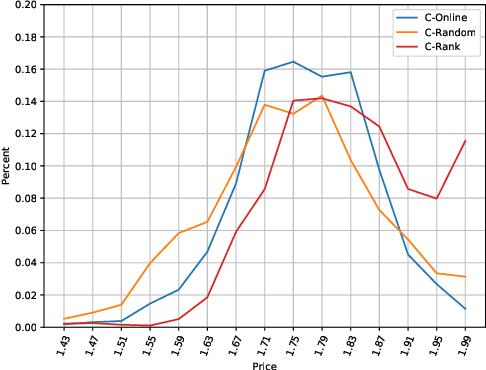

In an infinitely repeated pricing game, pricing algorithms based on artificial intelligence (Q-learning) may consistently learn to charge supra-competitive prices even without communication. Although concerns on algorithmic collusion have arisen, little is known on underlying factors. In this work, we experimentally analyze the dynamics of algorithms with three variants of experience replay. Algorithmic collusion still has roots in human preferences. Randomizing experience yields prices close to the static Bertrand equilibrium and higher prices are easily restored by favoring the latest experience. Moreover, relative performance concerns also stabilize the collusion. Finally, we investigate the scenarios with heterogeneous agents and test robustness on various factors.