Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeTi-MAE: Self-Supervised Masked Time Series Autoencoders

Paper and Code

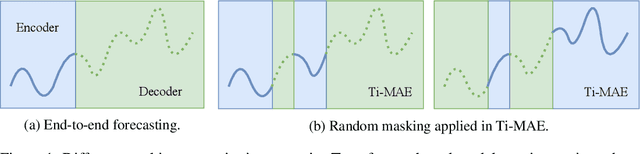

Multivariate Time Series forecasting has been an increasingly popular topic in various applications and scenarios. Recently, contrastive learning and Transformer-based models have achieved good performance in many long-term series forecasting tasks. However, there are still several issues in existing methods. First, the training paradigm of contrastive learning and downstream prediction tasks are inconsistent, leading to inaccurate prediction results. Second, existing Transformer-based models which resort to similar patterns in historical time series data for predicting future values generally induce severe distribution shift problems, and do not fully leverage the sequence information compared to self-supervised methods. To address these issues, we propose a novel framework named Ti-MAE, in which the input time series are assumed to follow an integrate distribution. In detail, Ti-MAE randomly masks out embedded time series data and learns an autoencoder to reconstruct them at the point-level. Ti-MAE adopts mask modeling (rather than contrastive learning) as the auxiliary task and bridges the connection between existing representation learning and generative Transformer-based methods, reducing the difference between upstream and downstream forecasting tasks while maintaining the utilization of original time series data. Experiments on several public real-world datasets demonstrate that our framework of masked autoencoding could learn strong representations directly from the raw data, yielding better performance in time series forecasting and classification tasks.