Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeStochastic Online Convex Optimization; Application to probabilistic time series forecasting

Paper and Code

Feb 01, 2021

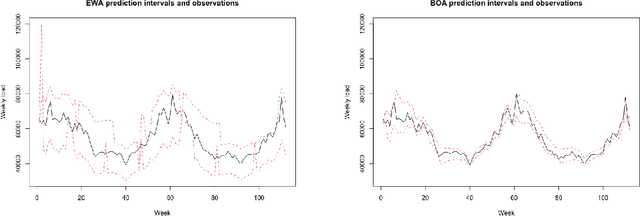

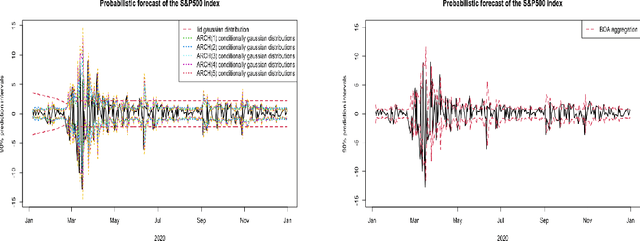

Stochastic regret bounds for online algorithms are usually derived from an "online to batch" conversion. Inverting the reasoning, we start our analyze by a "batch to online" conversion that applies in any Stochastic Online Convex Optimization problem under stochastic exp-concavity condition. We obtain fast rate stochastic regret bounds with high probability for non-convex loss functions. Based on this approach, we provide prediction and probabilistic forecasting methods for non-stationary unbounded time series.

View paper on