Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeSequential estimation of quantiles with applications to A/B-testing and best-arm identification

Paper and Code

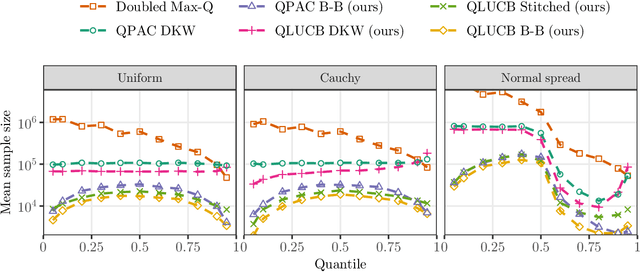

Consider the problem of sequentially estimating quantiles of any distribution over a complete, fully-ordered set, based on a stream of i.i.d. observations. We propose new, theoretically sound and practically tight confidence sequences for quantiles, that is, sequences of confidence intervals which are valid uniformly over time. We give two methods for tracking a fixed quantile and two methods for tracking all quantiles simultaneously. Specifically, we provide explicit expressions with small constants for intervals whose widths shrink at the fastest possible $\sqrt{t^{-1} \log\log t}$ rate, as determined by the law of the iterated logarithm (LIL). As a byproduct, we give a non-asymptotic concentration inequality for the empirical distribution function which holds uniformly over time with the LIL rate, thus strengthening Smirnov's asymptotic empirical process LIL, and extending the famed Dvoretzky-Kiefer-Wolfowitz (DKW) inequality to hold uniformly over all sample sizes while only being about twice as wide in practice. This inequality directly yields sequential analogues of the one- and two-sample Kolmogorov-Smirnov tests, and a test of stochastic dominance. We apply our results to the problem of selecting an arm with an approximately best quantile in a multi-armed bandit framework, proving a state-of-the-art sample complexity bound for a novel allocation strategy. Simulations demonstrate that our method stops with fewer samples than existing methods by a factor of five to fifty. Finally, we show how to compute confidence sequences for the difference between quantiles of two arms in an A/B test, along with corresponding always-valid $p$-values.