Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeSelf-boosted Time-series Forecasting with Multi-task and Multi-view Learning

Paper and Code

Sep 17, 2019

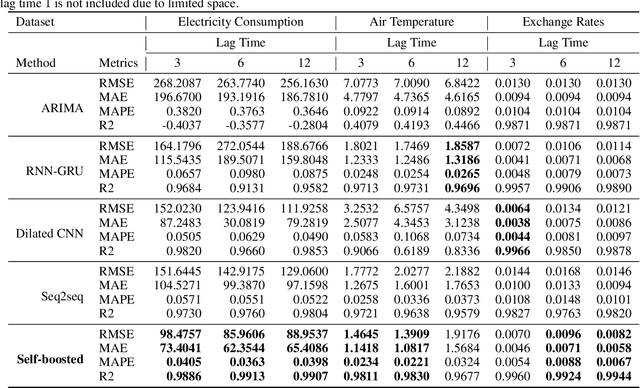

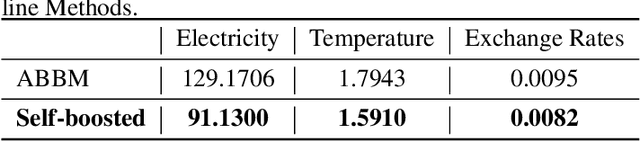

A robust model for time series forecasting is highly important in many domains, including but not limited to financial forecast, air temperature and electricity consumption. To improve forecasting performance, traditional approaches usually require additional feature sets. However, adding more feature sets from different sources of data is not always feasible due to its accessibility limitation. In this paper, we propose a novel self-boosted mechanism in which the original time series is decomposed into multiple time series. These time series played the role of additional features in which the closely related time series group is used to feed into multi-task learning model, and the loosely related group is fed into multi-view learning part to utilize its complementary information. We use three real-world datasets to validate our model and show the superiority of our proposed method over existing state-of-the-art baseline methods.