Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeRisk-aware Stochastic Shortest Path

Paper and Code

Mar 03, 2022

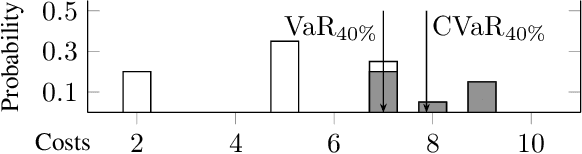

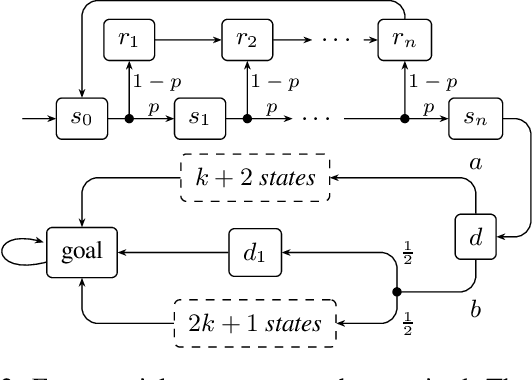

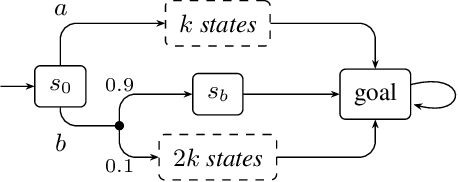

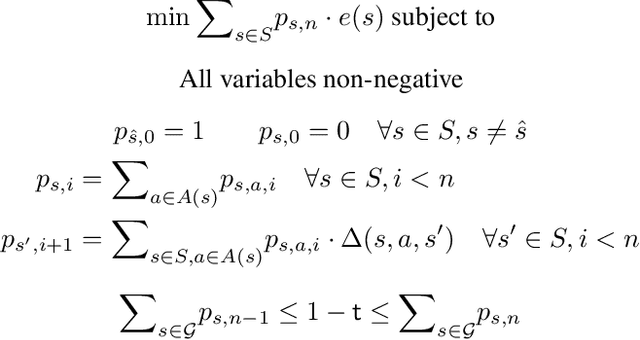

We treat the problem of risk-aware control for stochastic shortest path (SSP) on Markov decision processes (MDP). Typically, expectation is considered for SSP, which however is oblivious to the incurred risk. We present an alternative view, instead optimizing conditional value-at-risk (CVaR), an established risk measure. We treat both Markov chains as well as MDP and introduce, through novel insights, two algorithms, based on linear programming and value iteration, respectively. Both algorithms offer precise and provably correct solutions. Evaluation of our prototype implementation shows that risk-aware control is feasible on several moderately sized models.

View paper on