Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeRefinements of Barndorff-Nielsen and Shephard model: an analysis of crude oil price with machine learning

Paper and Code

Nov 29, 2019

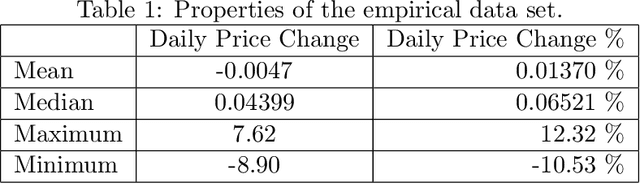

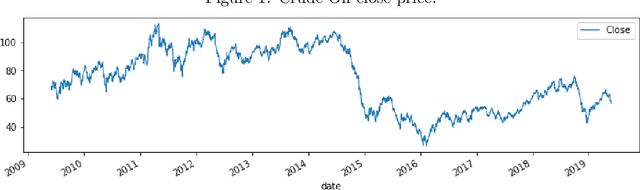

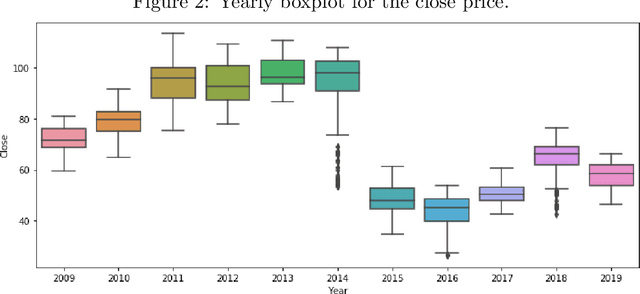

A commonly used stochastic model for derivative and commodity market analysis is the Barndorff-Nielsen and Shephard (BN-S) model. Though this model is very efficient and analytically tractable, it suffers from the absence of long range dependence and many other issues. For this paper, the analysis is restricted to crude oil price dynamics. A simple way of improving the BN-S model with the implementation of various machine learning algorithms is proposed. This refined BN-S model is more efficient and has fewer parameters than other models which are used in practice as improvements of the BN-S model. The procedure and the model show the application of data science for extracting a "deterministic component" out of processes that are usually considered to be completely stochastic. Empirical applications validate the efficacy of the proposed model for long range dependence.