Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgePlanning for the Efficient Updating of Mutual Fund Portfolios

Paper and Code

Nov 27, 2023

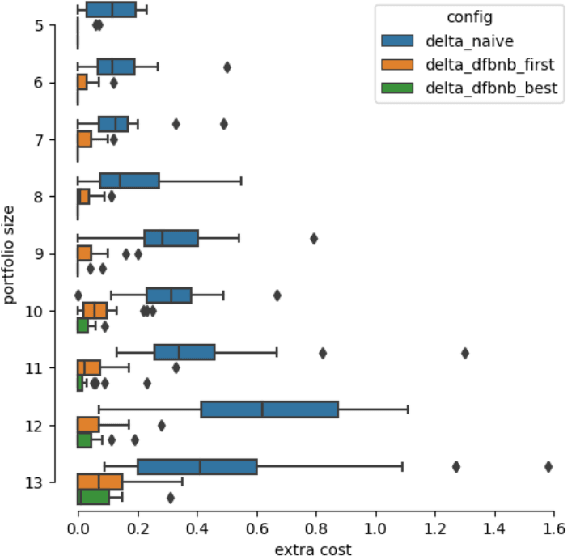

Once there is a decision of rebalancing or updating a portfolio of funds, the process of changing the current portfolio to the target one, involves a set of transactions that are susceptible of being optimized. This is particularly relevant when managers have to handle the implications of different types of instruments. In this work we present linear programming and heuristic search approaches that produce plans for executing the update. The evaluation of our proposals shows cost improvements over the compared based strategy. The models can be easily extended to other realistic scenarios in which a holistic portfolio management is required

* 8 pages

View paper on