Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeOnline Learning Algorithms for Statistical Arbitrage

Paper and Code

Nov 01, 2018

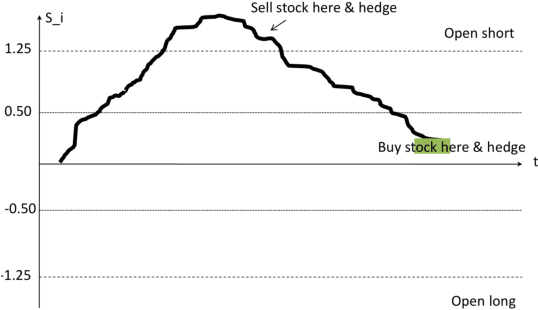

Statistical arbitrage is a class of financial trading strategies using mean reversion models. The corresponding techniques rely on a number of assumptions which may not hold for general non-stationary stochastic processes. This paper presents an alternative technique for statistical arbitrage based on online learning which does not require such assumptions and which benefits from strong learning guarantees.

View paper on