Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeMegazordNet: combining statistical and machine learning standpoints for time series forecasting

Paper and Code

Jun 23, 2021

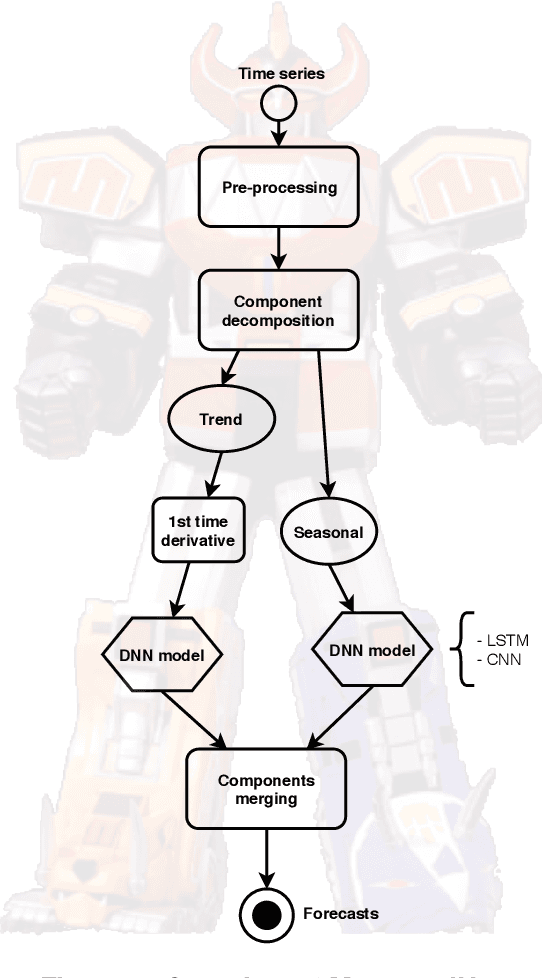

Forecasting financial time series is considered to be a difficult task due to the chaotic feature of the series. Statistical approaches have shown solid results in some specific problems such as predicting market direction and single-price of stocks; however, with the recent advances in deep learning and big data techniques, new promising options have arises to tackle financial time series forecasting. Moreover, recent literature has shown that employing a combination of statistics and machine learning may improve accuracy in the forecasts in comparison to single solutions. Taking into consideration the mentioned aspects, in this work, we proposed the MegazordNet, a framework that explores statistical features within a financial series combined with a structured deep learning model for time series forecasting. We evaluated our approach predicting the closing price of stocks in the S&P 500 using different metrics, and we were able to beat single statistical and machine learning methods.